Topics 27-30 Flashcards

(38 cards)

Describe and calculate the following metrics for credit exposure: expected mark-to-market, expected exposure, potential future exposure

- Expected mark to market (MtM) is the expected value of a transaction at a given point in the future. Long measurement periods as well as the specifics of cash flows may cause large differences between current MtM and expected MtM.

- Expected exposure (EE) is the amount that is expected to be lost if there is positive MtM and the counterparty defaults. Expected exposure is larger than expected MtM because the latter considers both positive and negative MtM values.

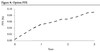

- Potential future exposure (PFE) is an estimate of MtM value at a specific point in the future. It is usually based on a high confidence level, taking into account the worst-case scenario. The current MtM may follow a number of different possible paths into the future, so a probability distribution of PFE can be derived, similar to the one shown in Figure 1. Positive MtM (the shaded area in Figure 1) is the part of the exposure that is at risk. Any points in this shaded area can represent PFE.

- In other words, PFE is the worst exposure that could occur at a given time in the future at a given confidence level. Potential future exposure represents a “gain” amount because it is the amount at risk if the counterparty defaults. Maximum PFE is the highest PFE value over a stated time frame.

Describe and calculate the following metrics for credit exposure: expected positive exposure and negative exposure, effective exposure, and maximum exposure

- Expected positive exposure (EPE) is the average EE through time. Expected positive exposure is a useful single amount to quantify exposure.

- Negative exposure, which is the exposure from the counterparty’s point of view, is represented by negative future values. The expected negative exposure (ENE) and the negative expected exposure (NEE) are the exact opposite of EPE and EE.

- The effective EE and effective EPE measures are meant to properly capture rollover risk for short-term transactions (under one year). Effective EE is equal to nondecreasing EE. Effective EPE is the average of the effective EE.

Compare the characterization of credit exposure to VaR methods and describe additional considerations used in the determination of credit exposure

The characterization of credit exposure is similar to the characterization of VaR, although additional considerations are relevant to credit exposure, described as follows:

- Application: Credit exposure is defined for both pricing and risk management, whereas VaR is just for risk management. As a result, quantifying credit exposure is more difficult and may result in different calculations for both pricing and risk management purposes.

- Time horizon: VaR models are based on a relatively short time horizon, whereas credit exposure must be defined over many time horizons. The trend (i.e., drift) of market variables, their underlying volatility, and their levels of co-dependence become relevant for credit exposure, whereas for VaR, these elements are irrelevant due to the short time horizon. Also, while VaR tends to ignore future contractual payments and changes such as exercise decisions, cash flows, and cancellations, credit exposure must take these elements into account because they tend to create path dependency (i.e., credit exposure in the future depends on an event occurring in the past).

- Risk mitigants: Netting and collateral are examples of risk mitigants, designed to reduce the level of credit exposure. In order to estimate future levels of credit exposure, these mitigants need to be taken into account. Netting requires that the proper rules be applied, which may add a level of complexity. Future collateral adds a significant element of subjectivity, as the type of collateral and time to receive collateral must all be modeled even though they may be unknown.

Identify factors that affect the calculation of the credit exposure profile and summarize the impact of collateral on exposure

The credit exposure profile is impacted by several factors, including:

- Future uncertainty: In situations where there is a single payout at the end of the life of a contract, uncertainty regarding the value of the final exchange increases over time.

- Periodic cash flows: Unlike the situation where there is a single payout, when cash flows occur regularly, the negative impact of the future uncertainty factor is reduced. However, additional risk exists when periodic cash flows are not equal in each period and are based on variables that may change as is often the case in an interest rate swap with variable interest rates.

- Combination of profiles: This exists when the credit exposure of a product results from the combination of multiple underlying risk factors. A cross-currency swap (which combines a foreign exchange forward trade with an interest rate swap) is a good example of this factor.

- Optionality: Exercise decisions (e.g., a swap-settled interest rate swaption) will have an impact on credit exposure. Collateral will also have a significant impact on credit exposure, as it typically reduces the level of credit exposure.

In addition, the reality is that risk is not removed entirely even with collateral due to factors such as delays in receiving collateral, variations in collateral value (i.e., when the collateral is something other than cash), the granularity effect (i.e., key parameters prevent asking for all of the collateral actually required), and the path dependency of collateral (i.e., the amount called for depends on the amount collected in the past).

Identify typical credit exposure profiles for various derivative contracts and combination profiles

- The PFE of bonds, loans, and repos are approximately equal to the notional value.

- Exposure profiles of swaps are typically characterized by a peak shape.

- The high volatility of FX rates, long maturities, and large final payments of notional value result in monotonically increasing exposures for foreign exchange products.

- Figure 8 provides an exposure profile for a long option position (with up-front premium) and illustrates the increase over time of the exposure until the option is exercised. The exact shape of the graph can change when the option is near, in, or out of the money. However, the increase over time is similar for all options due to the fact that the option can be deep in the money.

Explain how payment frequencies and exercise dates affect the exposure profile of various securities

Figure 10 illustrates that with unequal payments there is reduced exposure when payments are received more frequently than payments are made. Conversely, if a PFE were created for an interest rate swap where interest payments made were more frequent than interest payments received, it would have the reverse effect. In that case, the unequal payment PFE would show greater exposure than the equal payment PFE.

Explain the impact of netting on exposure, the benefit of correlation, and calculate the netting factor

It is also important to consider the relationship between netting and correlation. Positive correlations have lower netting benefits than negative correlations, with perfect positive correlation providing the least netting benefit. High positive correlations likely result in trades that are of the same sign, resulting in a small or zero netting benefit.

It is important to note that the netting benefit also depends on the initial MtM of transactions. For example, a trade with strong overall negative MtM under all scenarios will have a strong netting benefit by offsetting some or all of the positive MtM of other trades. Similarly, a trade with strong overall positive exposure under all scenarios will reduce the netting benefit by offsetting some or all of the negative MtM of other trades.

Explain the impact of collateralization on exposure, and assess the risk associated with the remargining period, threshold, and minimum transfer amount

When Party A has a positive exposure (e.g., receives cash flows in a swap transaction from Party B), Party A is said to have credit exposure because Party B could default.

When calculating an exposure profile, a risk manager should understand the factors that affect the collaterals ability to reduce risk. Specifically, factors that affect the calculation of exposure include thresholds, minimum transfer amounts, rounding, initial margin, and the remargin period.

The remargin period, also known as the margin call frequency, is the period from which a collateral call takes place to when collateral is actually delivered.

Steps that enter into the calculation of the number of days in the remargin period are as follows:

Step 1: Valuation/margin call: How long it takes to calculate current exposure to the counterparty and the market value of the collateral. These calculations help to determine if a valid call may be made.

Step 2 : Receiving collateral: The period between when the counterparty receives the request and when it releases the collateral.

Step 3 : Settlement: The time it takes to sell the collateral for cash.

Step 4: Grace period: The amount of time afforded to the counterparty obligated to deliver the collateral in the event that the collateral is not received by the requesting counterparty after the call. This may be a short window of time before the delivering counterparty would be considered in default for a failure-to-pay credit event.

Step 5: Liquidation/close-out and re-hedge: The time needed to liquidate the collateral, close out, and re-hedge positions.

Measuring Exposure During the Remargin Period

Potential disadvantages of PFE calculations

Potential disadvantages of PFE calculations include:

- It assumes a strongly collateralized position. PFE fails to work under a large threshold or minimum transfer amount, which produces a partially uncollateralized exposure.

- The analysis fails to account for the uncertainty of collateral volatility.

- Liquidity and liquidation risks are not considered.

- Volatility may differ from expected or implied volatility at the time of the collateral call and may not assume counterparty default.

- Wrong-way risk is not taken into account.

Collateral volatility

Collateral volatility must be calculated when a decline in the value of noncash collateral has the potential to create undercollateralization.

When there is no correlation between the volatility of the underlying exposure and that of the collateral, overall volatility is calculated as follows:

(variance of noncash collateral + variance of underlying exposure)0.5

This volatility measure would be used in the PFE formula to reflect the additive exposure of the collateral and volatility of the underlying exposure.

Modeling Collateral

Quantifying how much collateral reduces credit exposure is important. The risks that arise during the process of collateralizing exposure are:

- Collateralization may be deficient due to terms in the collateral agreement, such as threshold, minimum transfer amount, and rounding. These factors may result in less than full collateralization.

- Exposure could increase between margin calls. The increased amount of exposure may not be collateralized.

- Collateral is path-dependent. This means that the amount of collateral requested depends on how much was requested in the past.

Certain parameters impact the effectiveness of collateral in lessening credit exposure. These parameters are as follows:

- Remargin period: the time between the call for collateral and its receipt. The remargin period will be significantly longer than the actual legal margin call frequency; e.g., 10 days versus 1 day.

- Threshold: an exposure level below which collateral is not called. It represents an amount of uncollateralized exposure. The threshold represents an amount of uncollateralized exposure: If an exposure is above the threshold, only the incremental exposure will be collateralized

- Minimum transfer amount: the minimum quantity or block in which collateral may be transferred. Quantities below this amount represent uncollateralized exposure as well.

- Initial margin: an amount posted independently of any subsequent collateralization. This is also referred to as the initial margin. It is also called an independent amount.

- Rounding: the process by which a collateral call amount will be adjusted (rounded) to a certain increment.

Figuring out how much exposure should be collateralized at a given point in time involves several critical assumptions.

- Remargin period: how long before collateral is received from when it is first requested.

- Calculation of collateral called or returned: this exercise utilizes the aforementioned parameters.

- Calculation of collateralized exposure at each point in time: all amounts called for collateral less the remargin period.

Risk-Neutral vs. Real Probability Measures

- A risk-neutral parameter is often assumed in arbitrage pricing models where hedging is used. Conversely, when exposures are calculated for risk management purposes, the parameters are not risk-neutral but are based on real historical data and common sense. Parameters used for drifts and volatilities are market-driven (i.e., risk-neutral) and may not always reflect historical data or expected events.

- The length of data to use for parameter estimation has important implications. A shorter data sample window results in poor statistics, while a longer data sample window gives more weight to older, less relevant data.

SPV

A special purpose vehicle (SPV) is an off-balance sheet, bankruptcy-remote entity that can be created by various originators including investment banks and insurance companies. The general idea of an SPV is to create an entity that is separate from its originator but who holds such a high credit quality that default risk is theoretically negligible. Once created, an SPV will borrow money and purchase a series of assets from the originator. The SPV will then repackage the purchased assets into a structured note, like a collateralized debt obligation (CDO), and then sell these assets to investors. The originator will often need to provide a guarantee for the SPV as a counterparty. This may create a double default scenario where both the SPV and the originator are drawn into a counterparty solvency issue.

A special purpose vehicle, also sometimes called a special purpose entity (SPE), theoretically transforms counterparty risk into a type of legal risk. The legal risk is that a bankruptcy court might consolidate the assets of an SPV with their originator in the event of default. This would treat the SPV assets as if they had never been physically transferred off the originator’s books. This treatment will depend on jurisdiction, but U.S. courts have a history of consolidation rulings. Under this scenario, the goal of isolating the originator from counterparty risk with the SPV is often not realized.

DPC

A derivative product company (DPC) is an entity that evolved out of a need for over-thecounter (OTC) derivatives markets to manage counterparty risk. They commonly transact in credit default swaps (CDSs), equity derivatives, currency derivatives, and interest ratebased derivatives. A DPC is set up by a financial institution to obtain a AAA credit rating with separate capitalization from the originator. This puts further distance between a DPC and its originator. In this way, if the DPC originator were to fail, then the DPC would not be harmed. This provides a measure of enhanced protection for DPC counterparties.

Similar to an SPV, a DPC is established to be bankruptcy-remote from the originator. However, in the event of failure of the originator, a DPC is pre-arranged to either pass to another originator or to gradually unwind all mirrored transactions in an orderly fashion. Internal credit risk management guidelines also provide another layer of risk mitigation in a DPC. These restrictions often involve daily marking to market and collateral posting to limit risk exposures.

Monolines

A monoline insurance company (monolines) is a highly leveraged insurance company with a single business line to insure bond repayments. Their initial purpose was to enhance the credit quality of U.S. municipal issuers, but their pursuit of profit lead them to also offer credit enhancements, in the form of CDSs, for various structured credit products. Unlike a DPC, monolines do not post collateral against their transactions when business conditions are normal and they retain their AAA credit rating. This means that, in a normal state, losses are not formally booked through the marking-to-market process as they are with a DPC. However, if business deteriorates and the monoline’s credit rating is downgraded, then they may be forced to post collateral just at the time that their insured losses are mounting.

A case can be made that the monoline business model has been flawed from its inception. They operate as centralized entities that absorb systemic shocks by accepting large amounts of counterparty risk. One of the keys to risk mitigation is diversification, and monolines intentionally concentrate their insurance offerings, which works against the natural flow of risk mitigation.

CCP

- In the wake of the 2007—2009 financial crisis and the failure of the SPV, DPC, and monoline structure of counterparty risk intermediation, the central counterparty (CCP) has risen as a solution for systemic risk mitigation. CCPs provide clearing services for many different types of financial transactions between member firms, which means they essentially stand in the middle of previously bilateral OTC transactions and operate as the buyer for every seller and vice versa.

- CCPs remain market-neutral by netting all buy-side transactions with offsetting sell-side transactions. This multilateral netting process requires counterparties to post collateral through a margin account. The end result is less theoretical risk in the system due to the daily, or sometimes intra-daily, mark-to-market collateral system.

- In the event of a default, a CCP must replace non-performing contracts. This process is formally called novation, and it involves closing out the non-performing side of a bilateral contract with a new counterparty who is capable of meeting the contractual obligations. If the CCP does need to step in to resolve a defaulted contract, they may need to access default funds that are held on reserve by the CCP and fed by contributions by all member firms. In this way, the losses are mutualized among all member firms by the nature of the CCP’s structure. This loss mutualization process spreads any realized losses over a wide number of market participants rather than concentrating them with a singular party.

Describe the risk management process of a CCP and explain the loss waterfall structure of a CCP.

Should one of a CCP’s members default on a transaction, the CCP’s goal is to quickly terminate the transaction in an attempt to minimize realized losses.

- Their first action will be to attempt replacement of the defaulted contract with a valid contract from one of the CCP’s other members as the new counterparty.

- The first stage in the loss waterfall is for the defaulting member to sacrifice the collateral that they posted when their transaction was initiated and when daily marking to market occurred.

- The next layer down on the loss waterfall is the defaulting member’s default funds. In a perfect world, each member would contribute enough money to the CCP to pay for 100% of their potential losses, but this value could be prohibitively high. Instead of this high standard, members are required to contribute money into the CCP’s default fund at a level that would cover potential losses with a high confidence level.

- After the collateral and the default fund contributions from a defaulting member have been exhausted to remedy a realized loss, the CCP will dip into its own equity capital to a point where the CCP would still be able to function normally.

- If a loss still remains after these options have been exhausted, then the loss mutualization process takes over. The first layer of this process is to utilize contributions to the CCP’s default fund from the nondefaulting members.

- In extreme loss situations, member firms may need to make additional contributions to the default fund to prevent the CCP from total liquidation and collapse. These additional contributions are known as rights of assessment.

- If the needs of a CCP are significant, then it could be detrimental to the survival of the member firms. In this case, the CCP will either fail or require external liquidity support from a well-capitalized entity like a central bank. Full movement down the loss waterfall is an extremely low probability event.

Compare bilateral and centrally cleared over-the-counter (OTC) derivative markets

Key characteristics of bilateral markets include:

- Counterparty. In a bilateral market, the original counterparty remains in effect as long as the contract remains in effect.

- Available products. There are no limitations to products that can be utilized in bilateral markets. As long as the two parties agree to the terms of a contract, then it is able to be created.

- Contract netting. Any netting of contracts to offset risks will need to be manually and intentionally arranged by players in bilateral markets. Typically, trades are not offset as market participants are placing bets on specific events, which means they do not wish to be market-neutral.

- Eligible participants. Participation in bilateral markets is open to any and all market actors. The only exclusion would be if someone has such weak credit that no counterparty would be willing to take the opposite side of their trade.

- Concentration of counterparty risk. All contracts are willingly engaged between two bilateral parties. Through this process of self-selection, counterparties can actively choose to limit the risk of exposure to a given party.

- Collateral. Two bilateral counterparties are able to negotiate customized collateral arrangements. New regulatory rules are trying to standardize this factor, but for now, there is a great deal of flexibility.

- Close-out of default positions. Close-out of a default position can be messy in a bilateral market. This process is entirely between two bilateral counterparties and may quickly result in a default scenario for the entire counterparty and not just the isolated transaction.

Key characteristics of centrally cleared markets include:

- Counterparty. In a centrally cleared market, the original counterparty is effectively replaced when the CCP steps into the middle of the transaction. Through the CCP structure, the CCP becomes the new counterparty and the other CCP members become secondary counterparties.

- Available products. Financial products traded in centrally cleared markets must be standard, plain-vanilla (non-exotic), and liquid. This helps to limit loss potential from specialized contracts, but it also limits the flexibility of types of contracts that can be engaged in within the CCP structure.

- Contract netting. CCPs naturally try to remain market-neutral by netting financial transactions. This process helps to further spread out risk.

- Eligible participants. Centrally cleared markets are only open to clearing members, which are typically large financial institutions. Other entities may clear transactions by using a clearing member as a conduit only if they are willing and able to post the necessary collateral and a clearing member is willing to sponsor them.

- Concentration of counterparty risk. Since clearing members have a measure of protection to transact within the construct of a CCP, this does create an incentive for concentration of risk positions whereby a given CCP will see a meaningful percentage of the transactions for a given member firm.

- Collateral. A centrally cleared market has transparent collateral requirements and margin rules with daily or intra-daily posting. These rules are static and non-negotiable for member firms.

- Close-out of default positions. A coordinated default process is one of the hallmarks of a centrally cleared market. The loss waterfall is the heart of this process, and it has the potential to not let a default on a single asset result in the complete default of an individual member firm. This coordinated close-out structure helps to minimize internal costs due to operational efficiencies and also minimize legal risk because the member firms are already engaged in a rules-based transactional relationship.

CCP members (key types)

From the point of view of trading through a CCP, one can consider three types of participant:

- General clearing member (GCM) – a member of the CCP who is able to clear third parties as well as their own trades.

- Individual clearing member (ICM) – a member of the CCP who clears only their own trades.

- Non-clearing member (NCM) – an institution having no relationship with the CCP but which can trade through a GCM.

These relationships are illustrated in the figure below.

A GCM or ICM will typically be a large bank or dealer who has a large number of counterparties. An NCM is more obviously characterised by an end-user of OTC derivatives that may channel most or all of its trades through a single counterparty. By this counterparty being a GCM, the end-user can gain benefits from central clearing even though they are not a clearing member. Whilst these are the more obvious roles of members, they are not the only characterisations: for example, a GCM may in fact be another CCP and an NCM may be a smaller bank.

Assess the capital requirements for a qualifying CCP and discuss the

advantages and disadvantages of CCPs

Because a CCP is not risk-free, there are two specific capital charges that are applied to this system. The first capital charge is for trade exposure. This risk arises from the mark-to-market process along with potential future mark-to-market margin contributions that may be required. This exposure has a relatively small risk weight of 2%. The second capital charge is for default fund risk exposure. This risk comes directly from the loss waterfall whereby a member’s default fund contributions might be forfeited, non-defaulting members could have their default fund contributions captured due to the default of a member firm, and additional default funds may need to be raised using rights of assessment.

The advantages of a CCP include:

- Transparency. Unlike bilateral markets, a CCP can see aggregate risk concentrations because they are aware of many of the transactions of their member firms. This enables the CCP structure to potentially offset risks that it notices.

- Multilateral netting. The transparency of the CCP structure enables risk to be offset. The netting process eliminates the need for members to monitor the creditworthiness of other members. This process also lowers margin costs for member firms.

- Liquidity. Daily collateral settling leads to enhanced market transparency and therefore improved market liquidity.

- Legal and operational efficiency. Both netting and the collateral policies of a CCP increase operational efficiency and lower costs. Legal costs are also minimized due to the rules-based structure of a CCP.

- Loss mutualization. In the event that a CCP member defaults, the CCP will manage the default using the loss waterfall where realized losses may be shared by all members of the CCP. This reduces the market impact of a default scenario.

- Default management. The CCP also manages default scenarios with an orderly auction of the defaulted member’s position. This brings stability to the market and secures the best price possible for the market.

The disadvantages of a CCP include:

- Moral hazard. This well-known insurance industry concept can be applied to the CCP structure because there is little incentive for member firms to vet the creditworthiness of other member firms. The netting, collateralization, and loss mutualization process contribute to this view.

- Adverse selection. Most CCP member firms specialize in derivatives contracts. As such, they may have superior knowledge on pricing and risk compared to the CCP. This creates an environment where the member firms may choose to trade with CCPs that offer the best prices due to incomplete information.

- Bifurcations. The fact that CCPs are required to only clear standard contracts has created a bifurcated market where some trades are processed through clearing firms and some are not. This creates risks for the system.

- Procyclicality. Procyclicality refers to a positive correlation between an event and the state of the economy. As the market and economy become more volatile, CCPs generally increase collateral requirements, which can further exacerbate a potential default scenario.

Discuss the impact of central clearing on credit value adjustment (CVA), funding value adjustment (FVA), capital value adjustment (KVA), and margin value adjustment (MVA).

- During the 2007—2009 financial crisis, a good portion of the counterparty losses were not from direct defaults, but rather were from the impact of credit market volatility on bank earnings. As a result, Basel III established a credit value adjustment (CVA) charge to improve resilience to counterparty mark-to-market losses. The CVA is essentially a discount offered by a derivatives buyer to account for counterparty default potential. The use of centrally cleared CCPs greatly reduces counterparty risk and therefore reduces the CVA.

- Funding value adjustment (FVA) charges are costs associated with uncollateralized OTC derivatives contracts. Because CCPs require highly liquid collateral, traditional FVA charges are reduced by using a CCP structure.

- Regulators require that banks hold capital reserves to survive significant and unexpected credit risk events. When banks hold OTC derivatives contracts, the additional capital charge is called the capital value adjustment (KVA) charge. When a CCP is used to help insulate a bank from substantial losses, the KVA charge is reduced.

- Margin value adjustment (MVA) charges are related to direct costs of posting margin collateral on OTC derivatives contracts. Because CCPs require initial margin postings and daily marking to market (variation margin postings), the MVA costs have increased due to the centrally cleared CCP structure.

Distinguish between cumulative and marginal default probabilities

The cumulative default probability, F(t), represents the likelihood of counterparty default between the current time period and a future date, t.

The marginal default probability denotes the likelihood of counterparty default between two future points in time denoted t1 and t2.

Calculate risk-neutral default probabilities, and compare the use of risk-neutral and real-world default probabilities in pricing derivative contracts.

Risk-neutral default probabilities are calculated from market information, while real-world default probabilities are based on historical data. Typically, real-world default probabilities are less than risk-neutral default probabilities.

Risk-neutral default probabilities represent the estimated parameter value determined from an observable market price. If the pricing model is assumed correct, the unknown parameter can be determined by solving for the parameter value that makes the model price equal to the market price.

There may be other factors in addition to real-world default probability, such as a liquidity or default risk premium that are aggregated into the risk-neutral default probability calculation. Hence, the risk-neutral default probability is likely to overstate the actual probability of default.

risk-neutral default probability = liquidity premium + default risk premium + real-world default probability

The real-world default probability (i.e., actual probability of default by a counterparty) should be incorporated into quantitative risk and return assessment conducted during the risk management process. Risk-neutral default probabilities should be incorporated into hedging decisions because they are derived from actual market prices.