Probability Distributions Flashcards

(100 cards)

Probability distribution

A probability distribution lists all the possible outcomes of an experiment, along with their associated probabilities.

Discrete Random Variable

A Discrete Random Variable has positive probabilities associated with a finite number of outcomes.

Continuous Random Variable

A continuous random variable has positive probabilities associated with a range of outcome values–the probability of any single value is zero.

Set of possible outcomes of a specific discrete random variable

Finite set of values (in a discrete distribution, p(x)=0 if it cannot happened, and p(x)>0 if it can).

Probability Function

P(X=x) = p(x), such that 0<=1 and Σp(x)=1

Probability Density Function (pdf)

Function for a continuous random variable used to determine the probability it will fall in a particular range

Cumulative Distribution Function (cdf)

Discrete Uniform Distribution

Distribution where there are n discrete, equally likely outcomes.

Binomial Distribution

Probability distribution for a binomial (discrete) random variable that has two possible outcomes.

Probability of an outcome under a discrete uniform distribution

1/n

Probability of an outcome under binomial distribution (with p = probability of success)

Binomial tree

Illustrates the probabilities of all the possible values that a varaible can take on given the probability of an up-move and the magnitude of an up-move

Continuous Uniform Distribution

The probability of X occuring in a possible range is the length of the range relative to the total of all possible values. If a and b are the limits, then:

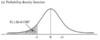

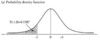

Normal Probability distribution

1) it is symmetrical and bell-shaped with a peak in the center

2) mean = median = mode,

3) the normal distribution is defined by the

mean and standard deviation; skew = 0; kurtosis = 3

Multivariate Distribution

Describes the probabilities for more than one random variable

Univariate Distribution

Describes the probabilities for a single random variable

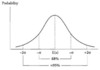

Confidence interval

The range within which we have a given level of confidence of finding a point estimate

90% confidence interval

μ +/- 1.65 standard deviations

95% confidence interval

μ +/- 1.96 standard deviations

99% confidence interval

μ +/- 2.58 standard deviations

Probability that a normally distributed random variable X will be within A standard deviations of its mean

Twice the cumulative left-hand tail probability F(-A), where F(A) is the cumulative standard normal probability of A

z-table

Used to find the probability that X will be less than or equal to a given value

P(X<>

P(X>x)