ERM Ch.3 Flashcards

(17 cards)

1

Q

IRM Components

A

- Startup: Staffing & Scope

- Parameter Development

- Implementation

- Integration & Maintenance

2

Q

Startup: Staffing & Score Components

A

3

Q

Parameter Development Components

A

- Modeling software – Assess the capabilities of the modeling software available, and make sure it matches capabilities of the IRM team

- Parameter Development – include expertise from Underwriting, Planning, Claims and Actuarial. Develop a systematic way to capture expert opinion

- Correlation – have the IRM team recommend correlations. This needs to be owned at a high level (CEO,CRO,CUO), since it crosses lines of business, and has a significant impact on the allocated capital.

- Validation‐ Validate and test over an extended period. Provide training, so that interested parties all have a basic understanding of the statistics

4

Q

Implementation Components

A

- Priority Setting – have top management set the priority for implementation

- Communications – Regular communication and to a broad audience

- Pilot Testing – allows effective preparation of the company for the magnitude of the change

- Education – training so leadership has a similar base level of understanding

5

Q

Integration & Maintenance Components

A

- Cycle – Integrate into planning calendar

- Updating – Major input review should be no more than twice a year; minor updates can be handled by modifying the scale of the impacted portfolio segments

- Controls – Maintain centralized control of inputs, outputs and even application templates

6

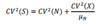

Q

Coefficient of Variation of the total losses

A

7

Q

Two ways to estimate Projection Risk

A

- Simple Trend Model

- Trend as a Time Series

8

Q

Estimation Risk

A

- Parameters are often estimated using the MLE

- Lowest estimation error of unbiased estimators

- Work with the negative of the second derivative of the log likelihook (information matrix - inverse of the covariance matrix)

- Slope is steep near the MLE - high confidence

9

Q

Why Joint LogNormal? (Small dataset problems)

A

- Standard deviations may be large ->Significant probability of having parameters w/ negative values

- For heavy tail distributions,, the parameters themselves are heavy tailed

10

Q

Model Risk - Selecting the best distribution

A

- Use the Hannan-Quinn Information Criterion (HQIC)

- It is a compromise of other information criteria which add larger or smaller penalties

11

Q

Select paramters for model risk

A

- Randomly select a mean for alpha and beta, and a covariance matrix from a pool of disributions you have selected

- Now that you’ve selected a distribution for alpha and beta, randomly draw an alpha0 and beta0

- For each claim that is simulated, draw from the distribution with parameters (alpha0,beta0)

12

Q

Kendall’s t

Concordant

Discordant

A

- t = (C-D)/# of pairs

- Concordant:

- x1>x2 and y1>y2 or vice versa

- Discordant:

- Mixed

- Focuses on rank of each data point not on its value

13

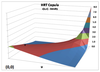

Q

Frank’s Copula

A

- Small tail dependencies

14

Q

Gumbel’s Compula

A

- More probability in the tails

- More density in the right tail

- t(a) = 1- (1/a)

15

Q

Heavy Right Tail (HRT) Copula

A

- Less correlation in the left tail, but high correlation in the right tail

- t(a) = 1/(2a+1)

16

Q

Normal Copula

A

- Joins two distributions using the correlations from the bivariate normal

- More dependencies in the tail

- Symmetrical

- t(a) = 2arcsin(a)/pie

17

Q

Tail Concentration Function - L & R

A

- L(z) = c(z,z)/z

- R(z) = (1 - 2z + C(z,z))/(1-z)