Swaps, Credit default swaps and Interest Rate Derivatives Flashcards

(39 cards)

Plain Vanilla Swap

Fixed for floating in the same currency

- Li (m)

- B0 (hj)

- M-day Libor on day i

- Present value factor on a zero-coupon instrument paying $1 on day j

Value of 1.0 in principal at hn - 1

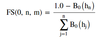

FS(0, n, m)

Fixed swap interest payment rate

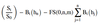

Present value of a series of fixed interest payments at the swap rate FS(0, n, m)

FS(0, n, m) price

*

Swap value on day t

- Fixed payments = FS(0, n, m) * Σ Bt (hj) + 1 * Bt (hn)

- Floating payments = [(Value of the first floating payment on day 0) + 1] * Bt (h1)

- Value of the first floating payment on day 0 = L0 (m) * (m/360)

- Value = floating payments - fixed payments

Swap value (pay fixed/receive equity return)

Swap value (pay floating/receive equity return)

(St / S0) - Value of the first floating payment on day 0 * Bt (h1)

CMT

Constant Maturity Treasury

OIS

Overnight Index Swap

Amortizing and accreting swaps are swaps in which the notional principal changes according to a formula related to the underlying

The more common of the two is the amortizing swap, sometimes called an index amortizing swap. In this type of interest rate swap, the notional principal is indexed to the level of interest rates

- Diff swap

- Arrears swap

- Capped swap

- Floored swap

- Combines elements of interest rate, currency, and equity swaps

- The floating payment is set at the end of the period and the interest is paid at that same time

- The floating payments have a limit as to how high they can be

- The floating payments have a limit as to how low they can be

Swaption

An option to enter into a swap

- Payer swaption

- Receiver swaption

- Allows the holder to enter into a swap as the fixed-rate payer and floating-rate receiver

- Allows the holder to enter into a swap as the fixed-rate receiver and floating-rate payer

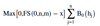

Payoff of a payer swaption

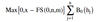

Payoff of a receiver swaption

Variation margin

Additional margin deposited on a futures to get back to the initial margin

Invoice price

Contract size x Futures settlement price x Conversion factor + accrued interest

Cheapest-to-deliver

The bond with the highest implied repo rate

Converted price

Futures price x Conversion factor

Delivery options of the short on a CBOT Treasury bond futures contract

- Quality or swap option

- Timing option

- Wild card option

Credit derivatives types

- Total return swap

- Credit spread option

- Credit-linked note

- Credit default swap (CDS)

CDS terminology

- Single-name CDS - on one specific borrower

- Reference entity - the borrower

- Reference obligation - the particular debt instrument

- Cheapest-to-deliver obligation - the payoff on which the CDS is based