Portfolio Management Flashcards

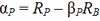

Arbitrage Pricing Theory (APT) - value of Ri

- the intercept is the expected return of asset i given that all the other factors take on a value of 0

APT assumptions

- A factor model describes asset returns

- There are many assets, so investors can form well-diversified portfolios that eliminate asset-specific risk, not factor risk

- No arbitrage opportunities exist among well-diversified portfolios

APT E(Rp) given that the 3 assumptions of the model hold

Pure factor portfolio (or factor portfolio)

A portfolio with a sensitivity of 1 to factor j and a sensitivity of 0 to all other factors

Carhart four-factor model notation (extension of the Fama and French model)

- RMRF = the return on a value-weighted equity index in excess of the one-month T-bill rate

- SMB = small minus big, a size (market capitalization) factor; SMB is the average return on three small-cap portfolios minus the average return on three large-cap portfolios

- HML = high minus low, the average return on two high book-to-market portfolios minus the average return on two low book-to-market portfolios

- WML = winners minus losers, a momentum factor; WML is the return on a portfolio of the past year’s winners minus the return on a portfolio of the past year’s losers

Carhart four-factor model / Rp - Rf

Carhart four-factor model / E(Rp)

Types of multifactor models

- Macroeconomic

- Fundamental

- Statistical:

- Factor analysis - best explain historical return covariances;

- Components models - best explain historical variances

bik for the fundamental factor model

Active return formula

- Asset allocation or sensitivity factor

- Security selection factor

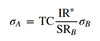

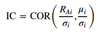

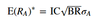

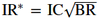

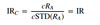

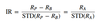

Information ratio (IR)

- = Active return / Active risk

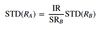

Active risk (also called Tracking error (TE)) - formula

- s(Rp - RB)

- s(RA)

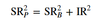

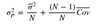

Active risk squared (active risk is also called tracking error or tracking risk) - formula

s2 (Rp - RB)

Active risk squared decomposition

- Active risk squared = Active factor risk + Active specific risk

- Active factor risk and active specific risk refer to variances rather than standard deviation

- Active factor risk

- Active specific risk or security selection risk

- The contribution to active risk squared resulting from the portfolio’s different-from-benchmark exposures relative to factors specified in the risk model

- The contribution to active risk squared resulting from the portfolio’s active weights on individual assets as those weights interact with assets’ residual risk

Portfolio alpha

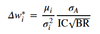

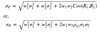

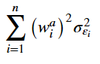

Active specific risk formula

Active specific risk notation

- wai is the ith asset’s active weight in the portfolio (that is, the difference between the asset’s weight in the portfolio and its weight in the benchmark)

- σ2εi is the residual risk of the ith asset (the variance of the ith asset’s returns left unexplained by the factors)

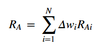

Value added formula

- RAi = Ri - RB

- Ri = return to asset i

- RB = return on the benchmark portfolio

- Δwi = wP,i – wB,i

Value added as the sum of the active asset allocation decisions and the weighted sum of the value added from security selection, RA,j = RP,j – RB,j, within each asset class

The first (parenthetical) term above is the value added from the asset allocation decision. The second term is the value added from security selection within the stock and bond portfolios. The active weights in the first term refer to differences from the policy portfolio

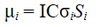

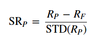

Sharpe ratio

Sharpe ratio for leveraged portfolio

- STD of the risk-free cash (1 - wp) is 0

- RC = wPRP + (1 – wP)RF

(Sharpe ratio)2p