Reading 53: Introduction to Fixed-Income Valuation Flashcards

(15 cards)

Present Value for Bond Price

(given market discount rate)

53.1

Intro to Fixed-Income Valuation

Present Value for Bond Price

(given sequence of spot rates)

53.2

Intro to Fixed-Income Valuation

Where:

Z1 = spot rate, or the zero-coupon yield, or zero rate, for Period 1

Z2 = spot rate, or the zero-coupon yield, or zero rate, for Period 2

ZN = spot rate, or the zero-coupon yield, or zero rate, for Period N

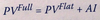

PVFull Equation

53.3

Intro to Fixed-Income Valuation

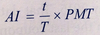

Accrued Interest

53.4

Intro to Fixed-Income Valuation

Where:

t = number of days from the last coupon payment to the settlement date

T = number of days in the coupon period

t/T = fraction of the coupon period that has gone by since the last payment

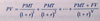

PMT = coupon payment per period

The full price of a fixed-rate bond between coupon payments given the market discount rate per period (r)

(PV Full expanded)

53.5

Intro to Fixed-Income Valuation

Similar to normal PV formula, but the difference is that the next coupon payment (PMT) is discounted for the remainder of thecoupon period, which is 1 - t/T. The second coupon payment is discounted for that fraction plus another full period, 2 - t/T.

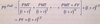

PVFull simplified

53.6

Intro to Fixed-Income Valuation

Uses PV

NOT PVFlat

Convert Annual Percentage Rate for m periods per year to APR for n periods per year

53.7

Intro to Fixed-Income Valuation

FRN Pricing Model

(required margin is discount margin)

53.8

Intro to Fixed-Income Valuation

Where:

PV = present value, or price of the floating-rate note

Index = reference rate, stated as an annual percentage rate

QM = quoted margin, stated as an annual percentage rate

FV = future value paid at maturity, or the par value of the bond

m = periodicity of the floating-rate note, the number of payment periods per year

DM = discount margin, the required margin stated as an annual percentage rate

N = number of evenly spaced periods to maturity

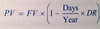

Pricing formula for money market instruments on a discount rate basis

53.9

Intro to Fixed-Income Valuation

Where:

PV = present value, or price of the money market instrument

FV = future value paid at maturity, or face value of the money market instrument

Days = number of days betseen settlement and maturity

Year = number of days in the year

DR = discount rate, stated as an annual percentage rate

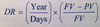

Formula for DR for money market instrument

53.10

Intro to Fixed-Income Valuation

Where:

PV = present value, or price of the money market instrument

FV = future value paid at maturity, or face value of the money market instrument

Days = number of days betseen settlement and maturity

Year = number of days in the year

DR = discount rate, stated as an annual percentage rate

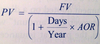

Pricing formula for money market instrumetn quoted on an add-on rate basis

53.11

Intro to Fixed-Income Valuation

Where:

PV = present value, pricipal amount, or price of the money market instrument

FV = future value, or the redemption amount paid at maturity including interest

Days = number of days betseen settlement and maturity

Year = number of days in the year

AOR = add-on rate, stated as an annual percentage rate

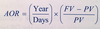

Formula for isolated AOR term

53.12

Intro to Fixed-Income Valuation

Where:

PV = present value, pricipal amount, or price of the money market instrument

FV = future value, or the redemption amount paid at maturity including interest

Days = number of days betseen settlement and maturity

Year = number of days in the year

AOR = add-on rate, stated as an annual percentage rate

Equation for calculating a par rate given a sequence of spot rates

(based on par curve)

53.13

Intro to Fixed-Income Valuation

Relationship between two spot rates and the implied forward rate

53.14

Intro to Fixed-Income Valuation

A = shorter-term bond periods to maturity

B = longer-term bond periods to maturity

zA = YTM per period on bond A

zB = YTM per period on bond B

The first is an A-period zero-coupon bond trading in the cash market. The second is a B-period zero-coupon cash market bond.

The implied forward rate between period A and period B is denoted IFRA,B-A

It is a forward rate on a security that starts in period A and ends in period B. Its tenor is B - A periods.

Zero Volatility Spread (Z-spread) of a bond over the benchmark rate

53.15

Intro to Fixed-Income Valuation

The benchmark spot rates z1, z2, …, zN are derived from the government hyield curve (or from fixed rates on interest rate swaps).

Z is the Z-spread per period and is the same for all time periods.

N is an integer, so the calculation is on a coupon date when the accrued interest is zero.