Quant: Time Value of Money Flashcards

(31 cards)

How do we start a TVM problem?

Draw a TIMELINE

Interest rates can be considered as…? (3)

Required rate of return (for compensation of risk) Discount rate (valuing future cash flows) Opportunity cost (of current consumption rather than saving)

nominal risk free rate =

real risk free rate + exp inflation rate - real risk free rate assumes no exp inflation

required interest rate on a security, r = [(5) factors]

real risk free interest rate + inflation premium + default risk premium + liquidity premium + maturity premium

EAR (Effective Annual Rate) =

EAR = (1 + periodic rate)^m - 1 where: periodic rate = stated annual rate/m m = the number of compounding periods per year –> stated rate and EAR will only be equal when the stated rate compounds ANNUALLY (m=1)

EAR (Convert annual stated rate to continuous compounding) =

= e^(annual stated rate) -1

FV =

= PV (1+ r)^n For a regular/simple investment the PV is the single cash outflow (principle invested)

FV (continuous compounding) =

= PV (e^[annual stated rate*n])

PV =

= FV / (1+r)n

Difference between an annuity, ordinary annuity and an annuity due

An annuity is a stream of equal cashflows that occurs at equal intervals over a given period. Ordinary Annuity is characterized by cash flows that occur at the end of each compounding period. The other type of annuity is called an annuity due, where payments or receipts occur at the beginning of each period (i.e., the first payment is today at t=0).

(an annuity due essentially has an extra period of interest earned)

Annuties: calculating FV & PV, Schw p106-108

For PV of an annuity, FV =

For an annuity where payment begins later than t =1:

For PV of an annuity, FV = 0

When payment begins after t =1, we have to do two steps (an ordinary annuity from the period before payment 1, and a regular discount back to t=0).

Calculating FV of an annuity due =

a) use BGN mode on calculator

b)

Calculating the PV of an annuity due =

a) use the beg mode in calculator

b) calculate PVAo (end mode) and multiply by the interest rate (to account for the extra interest earned)

PVAd = PVAo x (1+r), NB all else equal, the PV for an Ann Due is GREATER than PV for an Ord Ann

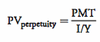

PV of a perpetuity =

Note that the PV of a perp is the value one period before the next payment.

FV of a cash flow stream (uneven, therefore not an annuity) =

Calculate the FV of each individual cash flow, the first one will have the greatest N (number of periods of compouding), and sum together. MAINTAIN CORRECT SIGNS (+/-)

PV of a (uneven) cash flow stream =

Sum the present value of each stream. N is larger for flows paid later.

OR use the NPV function on calculator

Loan Payment Calculation (paying pack principle + interest on an amortizing loan) =

The unknown is PMT (N equal payments)

Enter I, PV (-), N and assume FV = 0 to find PMT

Adjust as necessary for payments that aren’t annual (N will increase - NxY, I will decrease I/Y)

Breaking down interest and principal on a loan payment =

(NB. Need to clarify text on remaining principal)

Outstanding balance x I = interest portion

PMT - interest portion = principle portion

CAG (compound annual growth rate) =

Use TVM function, enter PV, FV and N to find I (when given a number of annual figures). The starting figure will be PV, the final will be FV.

Calculating payments to fund a future obligation (part 1)

Calculating payments to fund a future obligation (part 2)

Funding Future obligations: 2 Step (deposits made over period 1 to fund an annuity over period 2)

In calculating the amount required at year x for a 20 year annuity that will draw at the beginning of x, we can use TVM calculation with a) BGN, with N =20, or b) END, with N =19 and adding the PMT for year x in.

Present Value =

How much would have to be deposited now in order to make particular withdrawals in the future, exhausting the account with the final withdrawal?

Future Value =

How much would be in an account when the last of a particular series of deposits is made?