Unit 01: Basic Economic Concepts Flashcards

(66 cards)

01.02 Economic Basics

What is a Market Economy?

Questions are answered by the forces of supply and demand

- individuals own factors of productoin

- freedom to buy and sell

ex: USA

01.02 Economic Basics

What is a Command Economy?

Government makes decisions and own all factors of production

- no incentives take risks

- ex: Cuba, USSR

01.02 Economic Basics

What is the Traditional Economy?

Economic decisions dicated by traditions

- market forces not a factor

- third world nations

01.02 Economic Basics

What is a mixed economy?

Two or more types economies exist in one nation

01.02 Economic Basics

What is postitive and normative economics?

Positive Economics: way to look at economy → “what goods are produced”

Normative Economics: how things should be

01.02 Economic Basics

What are the factors of Production?

Hard answer questions → unlimited wants & scarce resources

Economics: study allocation scarce resources

01.03 Scarcity and Opportunity cost

What is scarcity and opportunity cost?

Economics → study overcome scarcity

- economic goods (hold value) are scarce (limited)

Scarcity → force make decisions and trade-offs = opportunity cost

“cost of choice make”

thing give up = opportunity cost (next best alternative)

- 3 options: second best → opportunity cost

01.04 Production Possibilities Curves

What is th Law of Increasing Opportunity cost?

Increase production of one goods, must give up increasing units of other

01.04 Production Possibilities Curves

Define Resource Sustainability

Resources in economy not adaptable to produce both goods

01.04 Production Possibilities Curves

What are the three types of curves of a PPC Curve?

Concave (bowing): indicates opportunity costs between two goods

- due to Law of Increasing Costs

Diagnonal Line: constant opportunity costs

Straight Line: no opportunity cost

- good parallel to line = free

01.04 Production Possibilities Curves

According to the production possibilities curve above, if the economy moves from point B to point E, the opportunity cost of each additional guava jelly

- increases.

- decreases.

- remains the same.

Increase

01.04 Production Possibilities Curves

According to the production possibilities curve above, which letter best represents an economy whose resources are not being fully utilized?

- A

- B

- C

- D

- E

4. D

01.04 Production Possibilities Curves

According to the production possibilities curve above, what is the opportunity cost of adding an additional 75 fishing boats in an economy that is already producing 75 fishing boats?

50 fishing boats

100 fishing boats

50 jars of guava jelly

100 jars of guava jelly

200 jars of guava jelly

1. 200 jars of guava jelly

01.04 Production Possibilities Curves

- If the production possibilities curve is concave from the origin, then economists say that

resources are scarce in the economy.

economic growth is occurring in the economy.

resources are not equally suited for the production of both goods.

resources are being inefficiently used in the economy.

resources are equally suited for the production of either good.

3. resources are not equally suited for the production of both goods.

01.04 Production Possibilities Curves

According to the production possibilities frontier above, a movement from the inside curve to the outside curve represents

- inefficiency in the economy.

- an unattainable point in the economy.

- economic growth in the economy.

- a decrease in resources

- a change from unemployment to full employment of resources in the economy.

3. economic growth in the economy.

01.04 Production Possibilities Curves

- If the production possibilities curve is a vertical line, then economists say that

- there are constant opportunity costs associated with these goods.

- resources are equally suited for the production of either good.

- the good on the X axis is a free good.

- the good on the Y axis is a free good.

- there are increasing opportunity costs for producing both goods.

4. the good on the Y axis is a free good.

01.04 Production Possibilities Curves

If an economy is operating at a point on the production possibilities curve, economists say that it is operating

below the full employment level of output.

above the full employment level of output.

at a level that is inefficient given the resources available.

at the full employment level of output.

at a level that is attainable but inefficient.

4. at the full employment level of output.

01.04 Production Possibilities Curves

Correct

All of the following will cause an outward shift of the production possibilities curve except:

New technology

Increased education of workers

An increase in productive resources

A decrease in population

Software advances

4.

A decrease in population

An example of an economic inefficiency in a nation is

- full employment.

- unemployment.

- opportunity cost.

- production possibilities.

- resources.

2. unemployment

01.05 Absolute and Comparative Advantage

Define Absolute and comparative advantage?

Absolute Advantage

Better at both tasks; who produces the most goods the fastest

Comparative Advantage

Lowest opportunity cost to produce something

01.05 Absolute and Comparative Advantage

What are the steps to determine comparative advantage?

Step 01: Divide the number of each product by number of product I for company A

Step 02: Divide the number of each product by number of product I for company B

Step 03: Divide the number of each product by number of product II for company A

Step 04: Divide the number of each product by number of product II for company B

Step 05: Determine which has to lowest opportunity cost for each product

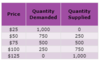

01.06 Demand

Define Demand:

Demand: when an entity is both (1)willing and (2)able to purchase an item.

01.06 Demand

What is Quantity Demaded?

Law of Demand:

Inverse relationship between price and quantity demanded (QD)

Influencing Factor: PRICE

- Determine if consumers buy more or less

What: Quantity demanded

- only moved point on curve (not curve as a whole)

- Inverse relationship with price