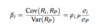

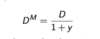

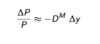

Formulas Revision Flashcards

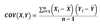

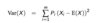

Variance

(With proba + with historical data)

Simple Interest=

X(1 + rT)

Future Value

X(1 + r)T

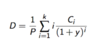

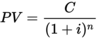

Present Value (2)

DF * X

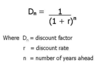

Discount Factor

PV of $1

Net Present Value

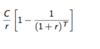

PV Perpetuity

PVp2 = value of a perpetuity paying C per year with first payment in T+1 years

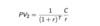

PV of an annuity: (3)

- PVp - PVp2

*

PV of an annuity paid at the beginingof the year

PVa * (1 + r)

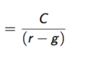

PVp with growth

PVa with growth

Effective Annual Rate

Effective Monthly Rate

Continuous Compounding

Xer

Continuous discounting

PV= Xe-rT

Real interest rate

(1+r)/(1+pi)

i=real interest rate

r=nominal interest rate

𝜋(pi)=inflation rate

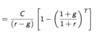

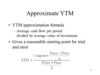

Approximate Yield To Maturity

Relationship formula YTM/PV

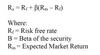

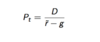

Gordon Growth Formula

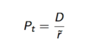

Stock Price with constant dividend

Return on Equity/Return on investment

= Amount of earnings a dollar of equity creates

EPS= earning per share

Earning growth

Plowback ratio = 1 -payout ratio

Nominal Interest rate =

Real rate + Inflation