Commodity Portfolio Management Flashcards

Commodity Characteristics

- Raw material or a primary agricultural resource, that can be purchased or sold for production and/or consumption.

- These tangible assets have no credit risks and many of them are most of time liquid.

- Commodities are traded on open markets throughout the world.

- Nearly no commodity price can go to zero, because commodities are always likely to be worth something to somebody. Only Power Prices have traded below 0.

1 Commodity BasicsBasics

1.1 Commodity Differentiation Basics

Physical Oil Market- 1.1 Commodity Differentiation Basics

1.1 Commodity Differentiation – Commodity Exchanges

1.1 Commodity Differentiation - Top Energy Products at the CME

1.2.1 Commodity Volatility

Driven by Supply and Demand, Inventories, Transport Costs, Logistics, Speculation, Sentiment, Geopolitical Factors.

1.3 Commodity Market Participants

The Actors on Commodity Exchanges

1.3.1 Types of Futures Market Participants

1.3.2 Commodity Trading Firms

1.4 Commitment of Traders Report

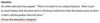

What does speculative participation look like as a fraction of open interest?

- The Commodity Futures Trading Commission (CFTC) publishes a weekly commodity futures/option report which breaks down the total open interest as of each Tuesday’s settlement.

-

The reports are released every Friday and provide market participants insight on how open interest is distributed among different groups of traders

- – (Producer/Merchant/Processor/User, Swap Dealers, Managed Money, and Other Reportable).

Open Interest

- number of long and short positions in a specific contract which have not been liquidated or offset by an opposing purchase or sale by the same participant.

- Non-commercials are momentum, or positive feedback traders

- commercials are on average contrarians (net short).

1.5 Open Interest

Open Interest

- number of long and short positions in a specific contract which have not been liquidated or offset by an opposing purchase or sale by the same participant.

- Increasing open interest figures are considered supportive of the underlying price trend.

– they may indicate market strength during periods of rising prices,

– or the support of a downward trend during periods of market weakness.

2 Rationale for Investing in Commodities

2.1 Diversification Benefits of Commodities

2.2 Commodities as a possible Inflation Hedge

3 Commodity Investment Vehicles

Commodity Assets Under Management by Type and Sector

- A niche asset class emerging from a cyclical downturn

3.1 Commodity Forwards

Value at Risk

The Benefits of Forward Curves

Term Structure of Commodity Prices

Arbitrage

3.1 Commodity Forwards–Synthetics

Basis Risk

3.1 Commodity Forwards–Several types of basic risk

3.1 Commodity Forwards–Financial Transaction Example: Power Station

3.2 Commodity Futures

• Future contract

– forward contract traded on an exchange

– standardized in terms of traded maturities, quantity of the commodity underlying the Future contract, and

– giving rise to physical delivery by the seller at maturity if not cash-settled contract.

- If the settlement is specified as financial, there must be a liquid reliable index to represent the underlying at date T (=maturity)

- Unlike an option, a Futures contains a_n obligation t_o buy (or sell).

- For both the buyer and the seller, the counterparty is the Clearing House of the Exchange.

• Long Futures Hedge -> you will purchase an asset in the future and want to lock in the price

- Short Futures Hedge -> you will sell an asset in the future and want to lock in the price

- Basis Risk:

– Difference between Spot and Futures

– Arises because of the uncertainty about the basis when the hedge is closed out

Typical pay-off structures of a futures contract

3.2 Commodity Futures–Initial Margin:

Margin: Example

3.2 Commodity Futures

• The Exchange must also provide information on

Futures prices of commodities that are investment assets such as gold and silver.

Example

3.2 Commodity Futures–Consumption Commodities

- Commodities that are consumption assets rather than investment assets usually provide no income, but can be subject to significant storage costs.

- We now review the arbitrage strategies used to determine futures prices from spot prices

- For some commodities the spot price depends on the delivery location.

- We assume that the delivery location for spot and futures are the same.

3.2 Commodity Futures–Convenience Yields

3.2 Commodity Futures–The Cost of Carry

Example

Spot Trading, forward contracts, future contracts

Exercise 1

Exercise 2

Exercise 3

Exercise 4

Exercise 5

Exercise 6

3.2.1 Price Discovery in Futures Markets

Commodity Futures have 3 Return Components

Commodity Futures Term Structure – Contango and Backwardation

Commodity Beta Return Drivers

Roll Yield vs. Returns

3.3 Commodity Options

Commodity Option: pay a small fee today (a premium) for the right (but not the obligation) to buy/sell a commodity at a predetermined price at a predetermined point in the future.

• Typically the underlying of an options contract listed on an exchange will be the futures

contract for the same commodity.

• Option contracts are also termed as call and put options based on the position of the

market participant when undertaking the contract.

- option gives the holder the right to do something.

- The holder does not have to exercise this right.

• This is what distinguishes options from forwards and futures, where the holder is

obligated to buy or sell the underlying asset.

• Whereas it costs nothing to enter into a forward or futures contract, there is a cost

to acquiring an option.

3.3 Commodity Options

Put option example

3.3 Commodity Options

Example: A gold manufacturer

Options pay-off

3.3 Commodity Options

Example: Call Option

Determinants of option premium?

Call option: Volatility

Option valuation

• As a European futures option has the same payoff as a European spot option when the

futures contract matures at the same time as the option, the model used to value

European futures options (lacks model) can also be used to value European spot options.

• However, American spot options and other more complicated derivatives dependent on

the spot price of a commodity require more sophisticated models.

• A feature of commodity prices is that they often exhibit mean reversion (similarly to

interest rates) and are also sometimes subject to jumps.

• Some of the models developed for interest rates can be adapted to apply to commodities.

Option Basics

Implied volatility

3.3 Commodity Options

Example: Seller of Call Option

Risk Analysis: why selling options?

• “Money talks”, get cash premium upfront

− If an API2 option is sold at 10 USD/MT for a tonnage of 75,000 tonnes the total premium

received is $750,000 now

• Long term view underlying market: bearish (sell call), bullish (sell put)

• Long term view volatility:

− An option seller sells option with the view that the volatility will reduce

• Possibility to hedge I arbitrage when linked to physical position

− It is less dangerous for a supplier who is naturally long to sell a call option

• Make sure risk management is in place before selling options

− Nick Leeson at Barings sold straddles and lost $1.4bn

− LTCM the option trader was one of the inventor of the Black Scholes model and he lost $3.7bn

Call Option: Application Physical Market

Call Option: Greeks—-Delta

Example: Put Option

Put Option: Application Physical Market

Example: Call Option Application

Selling Option Strangle

Collar

Hedging with Costless Collar

Hedging strategy of an oil consumer

Airline Fuel Hedging

Comparison to Forwards

Exercise 7

Exercise 8

Exercise 9

Question: Explain why margins are required when clients write options but not when they buy options.

Exercise 10

Question: Explain the difference between a call option on gold and a call option on gold futures.

Exercise 11

Question: Suppose you buy a put option contract on October gold futures with a strike price of $1,200 per ounce. Each contract is for the delivery of 100 ounces. What happens if you exercise when the October futures is $1,180?

Exercise 12

Question: Suppose you sell a call option contract on April live cattle futures with a strike price of 90cents per pound. Each contract is for the delivery of 40,000 pounds. What happens if the contract is exercised when futures price is 95cents?

Exercise 13

Question: Describe the terminal value of the following portfolio: A newly entered-into long forward contract on an asset and a long position in a European put option on the asset with the same maturity as the forward contract and a strike price that is equal to the forward price of the asset at the time the portfolio is set up.

Exercise 14

Question: A trader buys a call option with a strike price of $45 and a put option with a strike price of $40. Both options have the same maturity. The call costs $3 and the put costs $4. Draw a diagram showing the variation of the trader’s profit with the asset price

Exercise 15

Exercise 16

Exercise 1

Question: Explain why a short hedger’s position improves when the basis strengthens unexpectedly and worsens when the basis weakens unexpectedly.

Exercise 2

Exercise 3

Exercise 4

Question: Explain carefully the meaning of the terms convenience yield and cost of carry. What is the relationship between futures price, spot price, convenience yield, and cost of carry?

Exercise 5

Question: The spot price of silver is $15 per ounce. The storage costs are $0.24 per ounce per year payable quarterly in advance. Assuming that interest rates are 10% per annum for all maturities, calculate the futures price of silver for delivery in 9 months.

Exercise 6

3.4 Commodity Swaps

What is a swap?

Buying and selling swap

3.5 Commodity Index Investing

What is Commodity Beta?

Main contributor to total return was Collateral Yield

Roll Yield is quite volatile

Exercise 19

Question: Please explain the difference between hedging, speculation, and arbitrage.

Exercise 20

Question: Distinguish between the terms open interest and trading volume.

Exercise 21

Exercise 22

Exercise 23

Question: What is the difference between the forward price and the value of a forward contract?

Exercise 24

Exercise 25

Question: Explain why the futures price of gold can be calculated from its spot price and other observable variables whereas the futures price of copper cannot?

Exercise 26

Question: A futures contract is used for hedging. Explain why the daily settlement of the contract can give rise to cash flow problems.

Exercise 27

Exercise 28

Exercise 29