Risk and Return Flashcards

(13 cards)

Ways to measure Inflation

- CPI => Consumer Price Index, which measures the Purchasing Power of an average Citizen in the corresponding country

- The annual change in % of the CPI is called the Inflation

The nominal rate of return = real rate of return * expected Inflation

The Real Interest Rate

Equity Risk Premium (ERP)

- Average return of common stocks in the last 120 years: 11,5%

- Return of treasury bills (no risk alternative): 3,8%

- ERP = 11,5% - 3,8%= 7,7%

- It’s the premium, that can be earned by a long term investment in the stock market

- It’s earned by the willingness to take on stock market’s risks

- The EPR dependents on the historical data and the chosen time frame

Drivers of the ERP in different Countries

- Higher Risk in some countries (Italy)

- Higher Inflation in some countries

- Ex-Post some countries might have been more fortunate than been expected

- Valuation levels increases, based on dividend yield or M/B-ratio => Optimism => lower risk premium in the future

Measuring Risk, the Standart Deviation

- There is a difference between the expectation and the actual realization in any given year

- The return vary very much about the average over the last 100 years

- We can measure this spread with the standard deviation or the variance

how to calculate the variance a standard deviation of stocks

Variance:

Variance = 1/(n-1) Σ (rmt - rm)2

standart deviation is the square root of the variance

the bigger the variance, the higher the risk

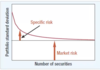

reducing risk through diversification

- the higher the diversification, the lower the standard deviation

- that’s because a some events are good for one company and bad for another, if you own both companies, the effects will smooth each other out

specific risk vs market risks

specific risks:

- the risk one events not benefitting the company => can be solved with diversification

market risk:

- you cannot get rid of this, because it will affect all companies

Correlation Measures of different stocks

- Covariance:

measures how 2 variables change together

covariance > 0 they move together

covariance < 0 move in opposite ways

covariance = 1/(n-1) Σ (rmt1 - rm1)*(rmt2 - rm1)

- Correlation coefficient

It is similar to the Covariance, but it only moves between 1 and -1

Correlation coefficient = covariance / ( SD1 * SD2)

calculating the risks and return of a portfolio

Expected return:

the weighted average of the expected return of all individual stocks

Portfolio risk:

the variance of portfolios with equal parts of all stocks

variance =

1/N*average variancestocks + (1-1/N)* average covariance

the bigger N gets the variance of the Portfolio becomes the average of the covariance, because the first part of the term gets close to zero, while the second multiplication becomes 1

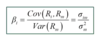

beta

- because a perfect diversified portfolio doesn’t have any specific risk only systematic or market risk.

- beta is the measurement of how stocks react to market risks

- beta=1 => the stock acts always similar to the market

- beta>>1 => the stock is very sensitive to the market, therefore you are getting a higher market risk

- beta is the slope of a regression model defined as: