Relevant Costs & Cost-Volume-Profit (Break Even) Analysis Flashcards

Relevant Cost Concept, An important concept when considering:

- Discontinuing a segment

- Make or buy decision

- Costing/pricing a on-off order

- Production scheduling with limited factor resources

The relevance of any cost depends on the situation under consideration.

•However, there are:

—Certain costs that are always relevant; and

—Certain costs that are always irrelevant

Costs that are always relevant :

- Variable costs (e.g. material)

- Direct costs (e.g. material)

- Opportunity costs (e.g. use of an existing equipment)

- Specific fixed costs (e.g. salary of a project supervisor)

Costs that are always irrelevant:

- Historic costs (e.g. the original cost of an equipment)

- Sunk costs (e.g. market survey)

- Committed costs (e.g. marketing contract that cannot be terminated early)

- General fixed costs (e.g. senior management’s salary)

General Fixed Costs:

- In terms of decision making, general fixed costs are irrelevant because whatever the decision, they will have to be paid (e.g. allocated head office fixed costs).

- Specific fixed costs that will only be incurred if the decision was to go ahead is relevant (e.g. resetting a machine for a specific order).

Sunk Costs

Sunk costs are always irrelevant.

Example:

An oil company has incurred £2m conducting exploratory studies to identify the best sites for drilling.

This is considered as an irrelevant cost to the current proposal to dig a well by the company.

What are Sunk Costs ?

A sunk cost is a cost that has already been incurred and thus cannot be recovered. A sunk cost differs from future costs that a business may face, such as decisions about inventory purchase costs or product pricing. Sunk costs (past costs) are excluded from future business decisions, because the cost will be the same regardless of the outcome of a decision.

Committed Costs

Committed costs are always irrelevant

(they are relevant if you are buying something regularly. However, the cost to use in the calculation should be the actual market price)

Example:

A company has already signed a one year lease agreement to a property to use as a warehouse. The cost of the lease is irrelevant when deciding whether to relocate the warehouse to a new location irrespective of whether the cost of the has already paid or not.

Opportunity Costs:

They are always irrelevant.

A proposal to make a newly-developed product offers an NPV of £3m.

An alternative is for the firm to sell the patent for £4m to another firm for it to make the product.

NPV £3m

Opportunity cost £4m

NPV (£1m)

Common costs are irrelevant while those costs which differ..

Between alternatives are relevant

DIFFERENTIAL COSTS/REVENUES

Ø Those costs/revenues which differ between alternatives

Ø Common costs are irrelevant

Ø Fixed costs are only relevant if they are specific or directly related to the particular decision being considered

Ø General fixed costs should be ignored since they will be paid anyway

Graph of Total Costs & Total Sales Against Activity

Definition of Break-Even Point

Ø The Break Even Point (BEP) is that point of activity (measured as sales volume) where total sales and total costs are equal

Ø So at BEP there is neither a profit nor a loss

Calcul: Total Fixed Cost / Contribution per unit

Profit Volume Chart

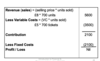

Contribution Per Unit :

Ø Contribution per unit is the sales price per unit minus the variable cost per unit.

Ø It measures the contribution made by each item of output toward the fixed costs and profit

Ø Referring back to the example:

Selling price per unit = £8

Variable cost per unit = £5

Contribution = £3

Break-Even Point in Pounds =

Break-Even Point in Units x Selling Price Per Unit

Contribution Income Statement

Determining Level of Sales to Cover Fixed Costs and Making a Profit

Break-Even Analysis for a Multi-product Company:

For multi-product company, it is not practical to calculate contribution per unit. So, we must use the contribution/sales ratio approach

BEP (£s of sales) = Fixed costs / CS ratio

To make a required amount of profit:

Amount to sell (£) = (FC + Required profit) / CS ratio

Contribution/Sales ratio =

CS ratio = Contribution / sales

Definition of Margin of Safety (MoS)

Ø The margin of safety is the difference between the break-even sales and the normal level of sales (measured in units, in £s of sales, or in %)

Ø The bigger the margin of safety, the better it is for the business.

Margin of Safety - Example

Ø Let us assume the following figures:

Ø Fixed costs = £32 000;

Ø Breakeven Point in units = 400 units

Ø Breakeven Point in sales £40,000

Ø Actual level of Sales in units = 500 units

Ø Actual level of Sales in £s £50,000.

Break-even analysis may be used to answer questions such as:

Ø What level of sales is necessary to cover fixed costs and make a specified profit?

Ø What is the effect of contribution per unit beyond the break-even point?

Ø What happens to the break-even point when the selling price changes?

Ø What happens to the break-even point when the variable cost per unit changes?

Ø What happens to the break-even point when the fixed costs change?

Limitations of Break-Even Analysis :Limitations of Break-Even Analysis

Ø The break-even graphs assume that cost and revenue behaviour patterns are known and change on a straight-line basis as activity levels change.

Ø It may not always be feasible to split costs neatly into variable and fixed categories. Some costs show mixed behaviour.

Ø The break-even graphs assume that fixed costs remain constant over the volume range under consideration.

Ø Break-even analysis, as described so far in this text, assumes input and output volumes are the same, so that there is no build-up of stocks and work-in-progress.

Ø Break-even charts and simple analyses can only deal with one product at a time.

Ø It is assumed that cost behaviour depends entirely on volume.