Economics: Macroeconomic Analysis Flashcards

Aggregate Output: GDP

Market value of all final goods and services produced in a country/economy.

- Produced during the period

- Only goods that are valued in the market

- Final goods and services only (not intermediate)

- Rental value for owner occupied housing (estimated)

- Government services (at cost)-not transfers

Aggregate Output: Calculating GDP - Income Approach

Earnings of all households + businesses + government

Expenditures Approach

Sum the market values of all final goods and services produced in the economy

OR

Sum all the increases in value at each stage of the production process.

Aggregate Output: GDP - Expenditures Approach

GDP = C + I + G + (X - M)

C = consuption spending

I = business investment )capital equipment + change in inventories_

G= goverment purchases

X = exports

M = imports

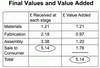

Aggregate Output: Final Values and Value Added

Aggregate Output: Nominal vs. Real GDP

Aggregate Output: GDP Deflator

Aggregate Output: National Income

GDP = national income

- +capital consumption allowance

- +statistical discrepancy

Capital consumption allowance is the output that goes to replace capital stock wearing out, depreciation

National income =

- employees’ wages and benefits

- +corporate and governmen tprofits pre-tax

- +interest income

- +unincorporated business owners’ income

- +rent

- +indirect business taxes - subsidies

(taxes and subsidies included in final prices)

Aggregate Output: Personal Income

Personal income=

national income

+ transfer of payments to households

- indirect business taxes

- corporate income taxes

- undistributed corporate profits

Aggregate Output: Personal Disposable Income

Personal disposable income

= personal income - personal taxes

= after-tax income

Each period, individuals decide whethr to consume or save disposable income

Aggregate Output: Deriving the Fundamental Relationship

GDP = C + 1 +G + (X - M) Total Expenditures

GDP = C + S +T Total Income

¢ + S + T = ¢ + I + G + (X - M)

S + T = I + G + (X - M)

S = I + (G - T) + (X - M)

Aggregate Output: Fundamental Relationship

S = I + (G - T) + (X - M)

Savings = Investment + Fiscal Balance + Trade Balance

Saving are either invested, used to finance government deficit, or used to fund a trade surplus, when both exist.

Aggregate Output: Income = Savings (IS) Curve

When income = planned expenditure:

(S - I) = (G - T) + (X - M)

Increase in income increases savings more than investment → (S - I) is an increasing function of income

Increase in income decreases fiscal deficit, increases imports → (G - T) + (X - M) is a decreasing function of income.

Aggregate Output: Deriving the IS Curve

Aggregate Output: IS Curve: Increase in real interest rate

When income = planned expenditure

(S- I) = (G - T) + (X - M)

Increase in real interest rate, holding (G - T) + (X - M) and (S - I) constant:

- Investment decreases

- Savings must also decrease

- Decrease in savings must result from decrease in income

Aggregate Output: The IS Curve

Aggregate Output: Equilibrium in the Money Market

Real money supply (M/P)

Money demand = f (real rates, income)

M/P = MD (r,Y)

Real rates up → quantity demanded down

Income up → quantity demanded up

Higher real interest rates → higher income

Aggregate Output: The LM Curve

Aggregate Output: The Aggregate Demand Curve

Aggregate Output: Aggregate Supply

In the very short run: Aggregate supply does not change (input quantities are fixed)

In the short run: input prices are fixed so businesses expand real output when (output) price increase

In the long run: Aggregate supply is fixed at full-employment or potential real GDP

Aggregate Output: Aggregate Supply Chart

Aggregate Output: Aggregate Demand

- The aggregate demand curve (AD) shows the relation between price level and real quantity of final goods and servies (real GDP) demanded

- Components of aggregate demand

- Consumption (C)

- Investment (I)

- Government spending (G)

- Net exports (X), exports minus imports

Aggregate demand = C + I + G + netX

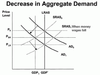

Aggregate Output: Shifts in Aggregate Demand

C + I + G + netX

- Increase in wealth increase C

- Increase in expectations for economic growth increase C, I

- Capacity utilization > - 85% increase I

- Increase in tax rates decrease disposable income and C

- I_ncreases in government spending_, G

- Increases in money supply reduce real rates and increase I, C

- Depreciation of currency increases netX - imports prices up, export prices down

- Growth of foreign GDP increases netX

Aggregate Output: Shifts in SR Aggregate Supply

Factors that Increase SRAS

- Descrease in input prices

- Improved expectation about future

- Decreases in business taxes

- Increases in business subsidies

- Currency appreciation that reduces the cost of imported inputs

Aggregate Output: Shifts in LR Aggregate Supply

Factors the Increase LRAS

- Increase in labor supply

- Increased availability of natural resources

- Increase stock of physical capital

- Increased human capital (labor quality)

- Advances in technology/labor productivity