week 3 Flashcards

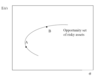

what is the opportunity set of risky assets?

The optimal CAL

The optimal CAL will be that which has a point of tangency with the opportunity set of risky assets; and,

Indeed, this tangency point represents the optimal risky portfolio, P, to mix with the riskless asset

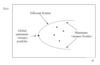

Markowitz Portfolio Selection

risk-averse investors can construct portfolios to optimize or maximize expected return based on a given level of market risk, emphasizing that risk is an inherent part of higher reward.

it’s possible to construct an “efficient frontier” of optimal portfolios offering the maximum possible expected return for a given level of risk.

The first step in this process, known as the Markowitz Portfolio Selection Model, is

determine the risk-return opportunities on offer

summarised by the minimum variance frontier of risky assets

efficient frontier shows

set of portfolios that maximise expected return for each level of portfolio risk

rational investors will choose a portfolio on the efficient frontier