Topic 2 - Financial Planning Skills Flashcards

What are the four important terms of considerations of investments?

Page 45

- Time value of money

- The effect of inflation and taxation

- Timing of cash flows

- Compounding frequency

Personal financial statements can be prepared in two parts:

Page 46

What do income and expenditure include?

When do you have net savings?

Pages 46-47

(002)

What does the personal balance sheet demonstrate?

What are assets, liabilities and net worth?

Page 48

The personal financial statements can be used to calculate the following useful financial ratios to analyse the family’s financial position:

Page 49

Calculate the net worth ratio:

Page 49

Calculate the liquidity ratio:

Pages 49-50

Calculate the savings ratio:

Page 50

Calculate the debt service ratio:

Page 51

- over 35% debt service ratio can indicate technical insolvency (not good!)

Why do people prefer cash now rather than later?

Page 53

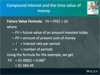

What is the compound interest of $1,000 invested for 4 years at 8% p.a.?

Study example on page 54

What is the future value (FV) formula?

Calculate the FV for $1,000 invested at 8% for 4 years.

Pages 54-55

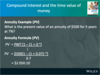

How much do we need to invest now at 8% to accumulate $1,360.49 in 4 years time?

Page 56

Note: The power of minus n is the reciprocal of the power of n, 1/n is the same thing as 1 exp -n or 1 to the power of minus n.

How much will we have at the end of 5 years if we invest $500 at the end of each year at 7%?

Page 57

What is the present value of an annuity of $500 for 5 years at 7%?

Page 57

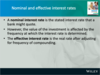

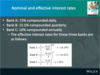

What’s the difference between the nominal and effective interest rate?

Pages 59-64

Since the time value of money formula assumes annual compounding, to obtain the periodic interest rate (i), an adjustment must be made:

Pages 60-61

What are the effective interest rates of the following three banks?

- Bank A: 15% compounded daily

- Bank B: 15.5% compounded quarterly

- Bank C: 16% compounded annually

* Page 62*

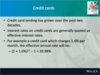

For a credit card that charges 1.6% per month, the effective annual rate will be:

Pages 62-63

What is the net present value (NPV) formula?

Pages 65-66

The holy grail of finance!

NPV is the present value of the future cash flows minus your initial outlay (investment)

Cannot be treated as an annuity because each cash flow is different (an annuity is identical each year)

How does the textbook define NPV?

What is missing in the definition?

Pages 65-66

- while the textbook covers the Sharpe ratio and the capital asset pricing model (CAPM), it doesn’t mention EMH

- if we don’t have efficient markets, the CAPM doesn’t work

a perfect market

- an infinite number of sellers and buyers

- everyone has perfect knowledge of the situation

- nobody can dominate the market

What is an efficient market?

What are the 3 forms of EMH?

What is an inefficient market?

EMH supplementary material handout

Efficient market

- how accurately and how quickly the market translates new information into the share price

3 levels of efficiency

Strong-form: stock market where news is accurately interpreted and instantly feeds into share price (non-existent)

Semi-strong-form: you can beat the stock market index by having (illegal) insider information (New York)

Weak-form: insider information is still valuable, but you can also beat the market by applying fundamental analysis of the firms - performance, solvency, reading the accounts, understanding the economics, becoming informed about a company’s competitive position (Tokyo, Hong Kong, London, Sydney)

Inefficient market

- slow to adjust to news, or misinterprets it

- may not be enough traders to buy/sell shares, or cartels keeping up the price

(022)

What is the weakness of the NPV technique?

Pages 65-66

- based on predictions

- predictions can be wrong - including the cost of capital (the discount rate itself)

- false security to rely exclusively on NPV when choosing between projects

If an investment costs $300 today and is expected to return $100 at the end of the next 4 years with an interest rate of 10% p.a., then the NPV is calculated as:

Page 66