Reading 55 LOS's Flashcards

(11 cards)

LOS 55a: Calculate and interpret the sources of return from investing in a fixed-rate bond

There are 3 sources of return from a fixed-rate bond:

- Receipt of promised coupon and pricipal payments

- Reinvestment of coupon payments

- Potential capital gains/losses if the bond is sold prior to maturity

A discount bond offers a coupon that is lower than the required rate of return

A premium bond offers a coupon that is higher than the required rate of return

In bonds we consider 2 types of investors:

Investor A buys and holds to maturity

Investor B - sells bond before maturity.

I_f interest rates remain unchanged_ through life of bond, investor A will realize YTM as their return given the bond is held to maturity, the issuer doesnt default, and all coupon payments can be reinvested at a rate that equals YTM. Investor B will also realize YTM as their return given that the bond is sold at its carrying value (refers to value of a bond that entails the same YTM as when it was purchased) and all coupon payments can be reinvested at a rate of YTM. If bond sells at different value than carrying value, investor B will experience capital gains/losses.

If interest rates rise investor A will experience a greater realized rate of return as the higher interest rates help earn more with coupon reinvestments. Investor B will experience a lesser realized rate of return, as the higher interest rates would lower the price of the bond when sold before maturity.

If Interest rates fall the reverse will be true from above.

As we can see investors face 2 risks:

Reinvestment risk The future value of any interim cash flows received from a bond increases with interest rate rises and decreases with interest rate falls (matters more to investor A, long-term investor)

Market Price Risk- the selling price of a bond decreases with interest rate rises and increases with interest rate falls ( matter more to investor B, the short-term investor.

LOS 55b: Define, calculate, and interpret Macaulay, modified, and effective durations

Duration measures the sensitivity or responsiveness of a bond’s full price to changes in its yield to maturity/ market discount rate.

Macaulay Duration represents the weighted average of the time it would take to receive all of the bonds promised cash flows, where the weights are calculated by dividing the present value of cash flows by the bond’s full price. ( So find present value of future cash flows, then divide these present values by bond price to get weights on payments. Then multiply these weights by the time period, and finally add these all up to get your duration.

There is also the closed form of the Macaulay Duration that involves a complex formula in the book.

The Macaulay Duration is normally not used as a measure of interest rate sensitivity but it does help in the measurement of the duration gap.

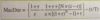

Modified Duration is simply the Macaulay Duration divided by one plus the yield per period. If the Macaulay is unknown, we can use the approximate modified duration, which uses points around our base yield and price, to figure out the slope of the tangent line. Important- this formula gives us the rate of change from 100 basis point movements (1%), if we were looking for sensitivity to 50 basis points we would divide by 2.

Modified duration also can be used in risk management to determine a bonds price sensitivity in response to a change in yield to maturity. Note the formula:

This formula uses annual modified duration and yield to maturity to find the full present value of a bond. An issue with this duration is that it measures price changes linearly, when we know that bond prices are subject to the convexity adjustment (increases in price due to decreases in yields are greater than decreases in price due to increases in yields)

Effective Duration (aka OAS duration)- this measures the sensitivity of a bond’s price to a change in the benchmark yield curve:

*Note- Effective duration is a curve duration in that it measures interest rate risks in terms of a change in yield curve, where as modified duration is a yield duration in that is measures interest rate risks in terms of changes to the bonds own YTM

Effective duration is the appropriate measure of risk for bonds with embedded call options

LOS 55c: Explain why the effective duration is the most appropriate measure of interest rate risk for bonds with embedded options.

Since bonds with embedded options future cash flows are unpredictable and contingent on future interest rates, there is no well define yield to maturity, thus the Macaulay and Modified durations (which are yield durations) are insufficient. These measures can be used only to determine durations on traditional fixed rate bonds.

NOTE- bonds with embedded calls can change in value if there is either a 1) fall in the benchmark price or 2) a decrease in the credit spread. Effective duration helps us understand the fall in benchmark price, but we will need another measure to consider credit spread.

LOS 55d: Define key rate duration and describe the key use of key rate durations in measuring the sensitivity of bonds to changes in the slope of the benchmark yield curve.

Key rate duration (or partial duration) is a measure of a bond’s sensitiviy to change in the benchmark yield for a given maturity. That is, it measures sensitivity to changes in the shape of the benchmark yield curve (or nonparallel shifts), differing from effective duration which measures parallel shifts in the yield curve. So if an analyst expected short maturities to rise by 25 bps, but remain unchanged at longer maturities, we would consider key rate change.

LOS 55e: Explain how a bond’s maturity, coupon, embedded options, and yield level affect its interest rate risk.

In terms of coupon payments, Macaulay durations fall from the last coupon payment to the next coupon payment, sharply jumping up when the next coupon payment arrives, and then repeating the process. This pattern looks like a “saw-tooth”. In general the longer the time to maturity, the higher the Macaulay duration. Premium Bonds will never cross the threshold of (1+r)/r, whereas discount bonds will reach a maximum above the threshold, and then gradually return to (1+r)/r.

Coupon Rate a lower coupon rate will have a higher duration than a high coupon

Yield to Maturity a lower YTM has a higher duration than a high YTM.

Callable Bonds here we will recall that Macaulay and modified durations can not be used to measure these bonds, instead we use the effective duration. When interest rates are high relative to the coupon rate, chances are the bond will not be called and the effective durations of the callable and noncallable will be very similar. When interest rates are low relative to the coupon rate, it becomes increasingly more likely the issuer will call the bond to refinance for lower. This makes the effective duration of a callable bond lower than that of a noncallable bond.

Putable Bonds- When interest rates are low relative to the coupon rate, it is unlikely the holder will put the bond back to the issuer, thus the duration of the putable and nonputable bonds are similar. When interest rates are high relative to the coupon rate, it is increasingly likely the holder will put, thus making its duration lower as its life expentancy becomes lower

LOS 55f: Calculate the duration of a portfolio and explain the limitations of portfolio duration

There are 2 ways to compute the duration of a bond portfolio:

1. Compute the weigthed average of time to receipt of the portfolio’s aggregate cash flows. For both tradional bonds and embedded bonds, the cash flows are aggregated to determine the portfolio’s cash flow yield (IRR based on projected cash flows). Though theoretically correct, this is difficult to do because:

- cash flow yield is not usually calculated

- amount of timing and payments for embedded options is uncertain

- interest rate risk should be measure by change in benchmark interest rates, not in cash flow yield

2. Compute the weighted average of the durations of the individual bonds held in the portfolio. This method considers the duration of each individual bond, and then finds the portfolio duration by multiplying the individual durations by a weight equal to the proportion of the individual bonds market value to the total portfolio’s market value. Though not theoretically correct, this method provides a good approximation. Advantages here are:

- bonds with embedded options can be calculated using effective duration, where as the previous method used Macaulay

- The computed value for duration can be used as a measure of interest rate risk

The disadvantage is that the measure of duration assumes a parallel change in the yield curve, when in reality, the portfolio can be composed of several different bonds subject to different yield curves

LOS 55g: Calculate and interpret the money duration of a bond and price value of a basis point (PVBP)

Money duration is very similar to modified duration. Where modified duration measures the percent change in the price of a bond to a change in its YTM, money duration is the measure of dollar price change in response to a change in YTM. So all you do is take your annualized modified duration and multiply it by the present value of the bond.

Price Value of a Basis Point- this is another version of money duration and it estimates the change in the full price of a bond in response to a 1-bp change in its YTM. The formula is as follows

A related statistic is Basis Point Value (BPV) which calculates how much a shift in basis point costs and the formula is

BPV= Money Duration * .0001

LOS55h: Calculate and interpret approximate convexity and distinguish between approximate and effective convexity.

LOS 55i: Estimate the percentage price change of a bond for a specified change in yield, given the bond’s approximate duration and convexity.

We know that price of a bond to its YTM is convex, yet the duration measure is linear. So for small changes in yield, duration measures are good approximations for interest rate sensitivity, but as the change in yield grows, these measures become less and less realiable. To deal with this, we simply need to revise our duration estimate using the convexity adjustment:

The first part of the last equation captures duration effect while the second part captures the convexity adjustment. Think of it this way, duration is the first derivative of the price-yield function, and convexity is the second derivative.

The above formulas deal with a fixed rate bond. To deal with embedded bond we use the formula :

Note that this formula uses the change in the curve squared where as the previous formula used the change in yield squared.

Negative Convexity (concavity) is an important feature of callable bonds. This concavity occurrs as benchmark yields decrease and the likelihood of the bond being called increases. At this point the embedded call option holds significant value to the issuer.

Finally note that putable bonds always have positive convexity.

LOS 55j: Describe how the term structure of yield volatility affects the interest rate risk of a bond.

Duration and convexity are useful measures in determing risk arising from changes in YTM, but the final piece of the puzzle is the term structure of yield volatility. Before we considered duration and convexity we assumed:

- The given change in yields was the same amongst securities and

- that there were only parallel shifts in the yield curve.

We know in practice these are not always the case.

Changes in bonds result from 2 factors:

- The impact per basis point change in the YTM, captured by duration and convexity

- The number of basis points in the change in YTM captured by yield volatility

LOS 55k: Describe the relationship among a bond’s holding period return, its duration, and the investment horizon.

We know that investors of bonds face 2 risks, 1) market price risk and 2) coupon reinvestment risk. Macaulay duration is actually a measure of when these 2 equal each other out. In other words we know that when interest rates fall, the price of the bond increases while the reinvestment of the coupons decreases. When interest rates rise the opposite is true. The Macaulay duration measures the amount of time for the losses to equal out the gains from either situation. This leads us to to be able to say 2 things:

- When the investment horizon is greater than the Macaulay duration, coupon reinvestment risk dominates market price risk, and the investor is concerned with falling interest rates

- When the investment horizon is less than the Macaulay duration, market price risk dominates reinvestment risk, and the investor is concerned with rising interest rates

This leads us to the measure of the duration gap:

- Duration gap = Macaulay Duration - Investment horizon

LOS 55l: Explain how changes in credit spread and liquid affect yield-to-maturity of a bond and how duration and convexity can be used to estimate the price effect of the changes.

A bond’s yield can change due to a change in the governments benchmark spread (composed of interest rate and expected inflation) and any changes in credit or liquidity. With that said we can use modified duration and convexity to estimate the change in the value of the bond from either changes listed above.