PM: Risk and Return 2 Flashcards

(27 cards)

Combining risk free and risky assets =

The optimal CAL (capital allocation line) =

best CAL is the one that offers the most preferred set of possible portfolios in terms of their risk and return.

different expectations of expected returns, standard deviations and correlation between risky assets will lead to different optimal risky asset portfolios and CALs.

Homogeneous expectations =

a simplifying assumption of modern portfolio theory is HOMOGENEOUS EXPECTATIONS - regarding expected returns, standard deviation and correlations.

as a result, all investors face the same EFFICIENT FRONTIER and have the same OPTIMAL RISKY PORTFOLIO and CAL

Optimal risky portfolio and CAL (given homogeneous expectations) =

optimal CAL is tangent to the efficient frontier.

all investors use the SAME PORTFOLIO OF RISKY ASSETS

but may choose different weights of risk free/risky assets

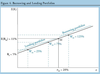

market portfolio (of risky assets) and the Capital Market Line =

all investors hold the same risky portfolio, the MARKET PORTFOLIO of all risky assets.

the optimal CAL for all investors is the CAPITAL MARKET LINE

along which EXPECTED PORTFOLIO RETURN is a LINEAR function of PORTFOLIO RISK

Capital Market LIne Equation =

y int: Rf, risk free rate

Slope: [E(Rm)-Rf]/SDm

so that if an investor takes no risk, SDp=0, the return is the risk free rate.

We can rearrange to get the below.

The investor will receive one unit of the market risk premium for accepting one unit of market risk, SDm.

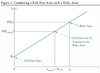

Borrowing and Lending portfolios =

Simple assumption that investors can both lend (invest) and borrow at the risk free rate - this means they can be invested at below or above the MARKET PORTFOLIO.

E(Rp) = Wm x E(Rm) + (1-Wm) x Rf

SDp = Wm x SDm

The market portfolio and active vs passive mgmt =

Those who think markets are not informationally efficient, and think their values/prices are more ‘correct’ than the market, will invest actively and not simply invest in the market portfolio.

an active manager will over and under weight securities based on their evaluation of value/price.

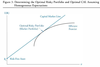

Systematic vs unsystematic risk =

the market portfolio contains all risky assets/has reduced all risk that can be reduced through diversification.

this is UNSYSTEMATIC RISK (unique, diversifiable, firm-specific)

this leaves SYSTEMATIC RISK (non diversifiable, market risk)

both portfolios and individual securities can have unsystematic and systematic risk

TOTAL RISK = SYSTEMATIC RISK + UNSYSTEMATIC RISK

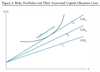

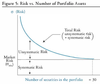

Risk vs # of portfolio assets =

Risk decreases at a decreasing rate when more securities are added to the portfolio - at a point the standard deviation will remain constant (12-18, 30, the number depends on the study)

Systematic Risk and the cost of diversification =

Capital market theory says

- equilibrium security returns don’t depend on total risk/SD, they depend on systematic risk

- Diversification is FREE

- thus, investors will not be compensated for unsystematic risk that can be reduced throught FREE DIVERSIFICATION

SYSTEMATIC RISK: is measured by the contribution of a security to risk in a well diversified portfolio

EXPECTED EQUILIBRIUM RETURN FOR A SECURITY WILL DEPEND ON ITS SYSTEMATIC RISK

Return generating and multi factor models =

RETURN GENERATING MODELS are used to estimate expected returns based on spefic factors.

A MULTIFACTOR MODEL uses macroeconomic, fundamental and (less so due to accuracy) statistical factors - with estimates of how sensitive a security is to changes in particular factors.

Multi Factor Model Equation =

expected return above the risk free rate = the sensitivity, or factor loading (Bs), x expected value of the factor for the period.

First factor is often E(Rm-Rf), the expected market return.

Fama and French Model (+Carhart) =

Fama and French multifactor model: firm size, firm book value to market value ratio, return on the market portfolio - risk free rate.

Carhart adds a fourth facto - price momentum using prior period returns.

Single factor/index model =

expected excess return based on on factor exposure to the market return, factor weight/sensitivity “BETA i”

Market Model - to estimate a security’s alpha and beta =

market model is a simplified form of a single index model.

intercept ALPHAi and slope coefficient BETAi are estimated from historical return data.

ALPHA is Rf(1-BETAi)

Expected return is ALPHAi +BETAi(E(Rm))

ei is a deviation from this expected return

factor sensitivity/beta for asset i measures how sensitive its returns are to the return of the overall market portfolio

BETA =

the sensitivity of an asset’s return to the return of the market index (in the market model context)

standardized measure of the covariance of the asset’s return with market return

SEE FRONT OF CARD FOR STARTING FORMULA, KNOW HOW TO CALCULATE BETA FROM THESE FORMULAS

Graphing beta and the SECURITY CHARACTERISTIC LINE =

Extra context: we would calculate beta by regressing asset returns and market returns against each other to get a line of best fit.

the slope of this line is the sensitivity of asset excess returns (dependent variable) to market excess returns (independent variable) = BETA

SECURITY CHARACTERISTIC LINE is this regression line, with slope COVim/VARIANCEm (the formula for beta)

CAPM Eqn and the SML (security market line) =

excess return is a function of systematic risk (this is the only risk we are compensated for) - so we can plot the two against each other –> these equations rearrange to the simple CAPM eqn (E[R] = Rf + B(Rmkt - Rf)

Comparing the CML and SML =

CAPM - definition =

an equilibrium model that predicts the expected return on a stock given

- the expected return on the market

- stock’s beta coefficient

- risk free rate

Using CAPM to estimate the cost of equity =

we can use the CAPM model to find the expected return for a security, which is also the REQUIRED RATE OF RETURN FROM INVESTORS aka THE COST OF EQUITY

as an extension we could combine this with the cost of debt and a capital structure breakdown to get WACC for a firm.

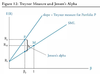

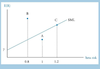

Valuations and plotting vs SML =

required return implied by beta risk vs analyst’s estimated return

A stock is OVERVALUED if the required return based on its BETA risk is GREATER than an analysts expected return for the stock. (vice versa for undervalued)

when a stock is OVERVALUED it plots below the SML line (which shows the E(R) based on B, or systematic risk)

ANY STOCK NOT PLOTTING ON THE SML LINE IS MISPRICED - an overvalued security needs to be cheaper so that the E(R) is compensating for the beta risk

Sharpe Ratio =

excess returns per unit of total portfolio risk

this is a slope measure - of the CAL (Capital Allocation Line) for the portfolio

Note that the slope of the CML is the sharpe ratio for any portfolio on the CML line.