Exam MFE Flashcards

(156 cards)

PCP for Stock

PCP for Exchange Options

Exchange Option Duality

C(A,B) = P(B,A)

PCP for Currency Exchange

Substitutions:

S ⇒ ?

r ⇒ ?

δ ⇒ ?

Bounds for Put Price

Rank the following:

- PEur 2. PAmer3. Max(0, Ke^(-rt) - FP(S) ) 4. K

K ≥ PAmer≥ PEur ≥ Max(0, Ke^(-rt) - FP(S) )

Bounds for Call Price

Rank the following:

- CEur 2. CAmer3. Max(0, FP(S) - Ke^(-rt)) 4. S

S ≥ CAmer≥ CEur ≥ Max(0, FP(S) - Ke^(-rt))

Rules for Early Exercise - American Call

Nondividend Stock = ?

Dividend Stock = ?

Nondividend Stock

Never Optimal

Dividend Stock

Optimal if PV(Divs) > PV(Int on Strike) + Implicit Put

Rules for Early Exercise - American Put

Nondividend Stock =

Dividend Stock =

Early Exercise is optimal if:

PV(Interest on Strike) > PV(Divs) + Implicit Call

Call Options Prices

Given K1 < K2 < K3, what 3 things do you know about call prices?

Put Option Prices

Given K1 < K2 < K3, what 3 things do you know about put prices?

An option can be replicated by buying ___ shares of the underlying stock and lending ___ at the risk free rate.

An option can be replicated by buying Δ shares of the underlying stock and lending B at the risk free rate.

Replicating Portfolio

Δ = ?

V = payoff of the option

Replicating Portfolio

B = ?

V = payoff of the option

Currency Exchange Duality

Replicating Portfolio

For Calls, Δ is (+/-) and **B **is (+/-)?

For Puts, Δ is (+/-) and B is (+/-)?

For Calls, Δ is (+) and B ** is (–**)?

For Puts, Δ is (–) and B ** is (+**)?

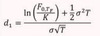

Risk Neutral Probability Pricing

p* = ?

Risk Neutral Probability Pricing - Option Price Formula

Option Price (V) = ?

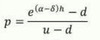

Realistic Probability Pricing

p = ?

Realistic Probability Pricing

Option Price (V) = ?

Realistic Probability Pricing

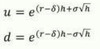

Forward Tree

If u and d are not given,

u = ?

d = ?

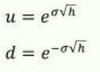

Cox-Ross-Rubinstein Tree

u = ?

d = ?

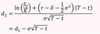

Lognormal Tree (Jarrow-Rudd Tree)

u = ?

d = ?

In the Binomial model, how can you tell if arbitrage is available?

Arbitrage is available if the following inequality is not satisfied: