economics-micro Flashcards

What is economics?

Economics is a social science that studies how humans make decisions when they face scarcity.

What does scarcity mean?

Scarcity means that our wants and needs are greater than the amount of available resources.

Economic agents make decisions based on:

- Political Judgement<br></br><br></br>- Short term outcomes<br></br><br></br>- Moral Judgement<br></br><br></br>- Normative Statements

What is a positive statement?<br></br>

They are objective statements that can be proved by referring to evidence

What is a normative statement?

They are statements of opinion that contain a value judgement

What is a value judgement?

They are judgements about society that cannot be quantified and tested, found within a normative statement.

What does ceteris paribus mean?

all other things kept equal.

How is economics Similar to other sciences?

- Develop theories and make models<br></br><br></br>- Use economic models to make predictions<br></br><br></br>

How is economics different to natural sciences?

- Controlled approaches experiments cannot be conducted<br></br><br></br>- economist use the assumption ceteris paribus<br></br><br></br>

What is the basic economic problem?

There are not enough resources on earth to satisfy humans’ unlimited wants and needs.

What are the 3 foundations to economics decisions?

What to produce?<br></br><br></br>How to produce?<br></br><br></br>Who to produce for?<br></br><br></br>

What is a need?

something necessary for survival e.g food, water, shelter

What is a want?

Things people can live without but desire e.g luxury cars, designer clothes

What are the 4 factors of production?

land, labor, capital, enterprise

What is meant by land?

Finite and non-finite resources found on the planet, including animals, water and natural materials.

What is meant by labour? (2 things)

Human capital - the value human labour brings to the production process<br></br><br></br>Labour force - the population that can work.<br></br><br></br>

What is meant by capital?

Human made resources: technology machinery

What is meant by enterprise?

The entrepreneurs who take a risk to make a profit by creating things from the other factors of production.

What are the 3 main economics agents? What are their roles?

- Producers: supply goods/services<br></br>- Consumers: purchase goods/services<br></br>- Governments: Establish rules in an economy

What decisions does a producer make?

Producers must decide what products to make and the selling price of products.

What decisions does a consumer make?

Consumers decide what products to purchase and how much they want to spend on products.

What is an opportunity cost?

The loss of potential gain from other alternatives when one alternative is chosen.<br></br><br></br>

What are some problems with opportunity cost?

- Not all factors have alternatives<br></br>- Some alternatives are unknown<br></br>- Agents may lack information on alternatives

What is a trade-off?

sacrificing one good or service to purchase or produce another

-it explains the constraints experienced by society.

- As we increase the production of Good X the more of Good Y has to be sacrificed

- Improvements in labour and technology

- Increased resources (increase in total number of workers)

- A loss of resources (e.g. natural disaster)

- Migration

Products are produced at a level where average costs are at their lowest

This is because your opportunity cost is greater towards the end of the PPF

Rise in price = Contraction

Fall in price = Extension

I - Income

R - Related goods (subs and complements)

A - Advertisement

T - Tastes

E - Expectations (future price change)

S - Season

For inferior goods, increased increased income will lead to a fall in quantity demanded (Rice)

- Upwards sloping demand curve.

- Upwards sloping demand curve.

Any price increase will cause demand to drop to zero.

- Decreasing price means firms are unable to cover costs.

Any price change won't affect demand.

- 0 < YED < 1

- (income rises, demand increases).

Increasing price = decreases total revenue.

Increasing price = increases total revenue.

- When PED is elastic the firms will take up the burden, since increasing the price will cause a large fall in demand

- Necessity Goods

- Addictive habit forming goods

- Substitutes

- Brand Loyalty

- Income % spent

- Time (SR vs LR)

Cheap - Price inelastic

At midpoint : unit elastic

At zero price/high quantity : price inelastic

PED of ± 1 = maximised total revenue.

Decrease price - contraction

I - Indirect taxes

N - Number of firms

T - Technology

S - Subsidies

W - Weather

C - Costs of production

OR

A change in the cost, quality or quantity of factors of production.

- Improve technology

- Flexible working patterns

Refers to a period of time in when at least one factor of production is fixed, usually capital.

Long run = Elastic. Firms can increase capacity as all factors are variable and have longer to react.

- Spare production capacity

- Artifcial Limits

- Factor mobility

- Time

- This is the only price where the amount consumers want to buy is equal to the amount producers want to sell.

- Supply and demand are independent from each other

- All markets are perfectly competitive

- A decrease in demand will cause the price to fall. Supply will contract and form a new equilibrium.

- A decrease in supply will cause an increase in price. Demand will contract and form a new equilibrium.

2. Firms incentivesed to change price

3. Rations away excess demand/supply

4 Allocates resources effectively

- Land

- Labour

- Capital

- Enterprise

- More training

- More education

- Reduce cost of training

- Increase labour productivity

- bored workers

- over reliant on 1 firm

- then falls because fixed factors of production constrain production

- for example a pizza shop with 5 ovens wouldn't benefit from from adding 6

or 7 or 8 workers

- this all happens because of the law of diminishing returns

- Total product is maximised when adding an extra factor input doesn't change output in any way

- Better management

- Improved technology

When MC falls, MP is rising

MC = change in TC ÷ change in quantity

When marginal cost > average cost = average cost is increasing.

When marginal cost > average cost, average cost is increasing.

So MC can only cut AC when the AC is neither increasing or decreasing, the lowest point. (MC=AC - Productive efficiency)

- Variable cost vary with output

2. Initially AFC is falling as TFC is spread across more output and AVC is falling as workers specialise and begin to take advantage of underutilised capital

3. When LoDM kicks in my AVC rises as fixed factor cause a contraint to my variable factors

4. This will offset the effects of my AFC falling and cause AC to rise, explaining why it is 'U' shaped

So you dividing a constant number by a number that is always increasing

What is economies of scale?

(cost benefits of operating on a larger scale)

- If one part is not successful, they have other parts to fall back on. can help lower average costs

eg Major pharmaceuticals companies, such pfizer inc, all undertake research in developing new drufe

- Silicon Valley outside San Francisco has become a hotspot for IT related industries. This attracts skilled workers. Firms have to spend less on recruiting skilled labour

- Ruhr valley in Germany has many chemical firms, meaning that are supplies and transport links related to the industry

- Communication becomes more difficult, with an increasing number of staff

- Worker alienisation: Wokers may feel unomotivated in a large workforce, leading to decreased productivity

- Managers may be less able to control as workforce increases

2- Physical resource competition, driving raw material prices up

3- Infrastructure competition eg transport congestion

Think hip

- This can force other firms out of business and cause a monopoly

- Increasing all factors of production leads to a more than proportional increase in output.

- increasing all factors of production leads to a less than proportional increase in output

- Increasing factors of production will lead to a proportional increase in output

- Decreasing returns to scale contributes to diseconomies of scale

- This is the lowest level of output where full EoS can be exploited and after this point a firm no longer receives EoS

- Eventually they can increase their factors of production until they are confined again by a fixed level of factors of production

- this continue and makes multiple SRAC curves which make up the LRAC curve

- However as they continue to increase factors of production become harder to manage and coordinate properly, so average costs increase

- So in the short run cost can be reduced to this minimum level as some factors are fixed

TR = Q x P

AR = TR ÷ Q

MR = change in TR ÷ change in Q

= P x Q ÷ Q

= P

- The curve is horizontal when there is perfect competition as the firm is a price taker so demand is perfectly elastic

- The firm must take the price set by the market and any increase in price will cause quantity sold to drop to 0

- So when AR is constant TR increases proportionally with sales.

- total Revenue = Price x quantity of output

- each point on the curve represents the price of the product in the market.

- Price determines the demand for a product, hence average revenue curve is also demand curve.

- When MR is negative every additional sale brings less revenue so TR is decreasing

- TR can only be maxed when MR is neither increasing or decreasing so it is maxed when MR = 0

Normal profit is when AC = AR (0 opportunity cost)

AC > AR

AR > AC

- If marginal cost is less than marginal revenue, the firm could increase profit by expanding production.

- If marginal cost is greater than marginal revenue, the firm could increase profit by reducing output.

Accounting profit only considers explicit costs.

- so they will continue to produce with prices below AC as long as they cover AVC so fixed cost can start to be payed off

- An innovation involves putting that advancement to use in a new product or service.

- It describes the continuous process of innovation and change in a capitalist economy, where new technologies and business models disrupt and replace older ones, leading to the destruction of existing companies and industries.

- For example, the rise of online retailers like Amazon has led to the closure of many brick-and-mortar stores, but has also created new jobs and consumer benefits such as lower prices and greater convenience.

- YED > 1

- Price discrimination

- Creating a more inelastic demand

- This means the price mechanism leads to a price and quantity that isnt best for society.

M\(^2\)PIIE

- A partial market failure occurs when a market supplies a good, but at the wrong quantity and/or the wrong price e.g. education

- The are non-excludable & non-rival

- e.g. if I pay to use a streetlight, I cant stop someone walking behind me from using it aswell

- e.g. if I pay to use a beach, it doesnt reduce the quantity available to others

- This could lead to a complete market failure as the market would not provide the public good

- If there is alot of traffic on a road it can become rival as the road has been used by the other drivers

- Parks

- Beaches

- Then when the American and Canadians developed new boats that allowed them to carry more fish, the amount of fish they caught was greater than the rate that the fish were reproducing

- Today there is only 1% of the total cod that there was in the 70's

- If the government are the only providers this reduces choice and quanitity, which can result in productive, allocative and dynamic inefficiency leading to government failure

- Vast opportunity cost the government suffer

- Lack of profit motive can lead to X-ineffiecny and diseconomies of scale

- In some cases, might be effienent for the government to fund but the private sector to provide certain public goods eg. prisons

- They make sure that essential public goods such as healthcare and education are provided as they provide positive externalities. The free market may struggle to provide these goods due to the free rider problem leading to a market failure

- Lack of pofit motive makes public goods affordable- this is important for equity

- Helps develop long term growth and economic development through the provision of infastructure

Social costs = Private costs + External cost

Social benefits = Private benefits + External benefits

On the right external costs are increasing for each unit produed

- Reduce consumption of goods by having legal ages e.g. alchol, smoking

- Reduce production of goods if they do not meet certain criteria e.g. cars

- Asymmetric information

- Used phones

- Private healthcare

If this outways the high prices consumers pay in the short run there will be no marlet failure.

- Occupational immobility leads to structual unemployment, which can cause a labour market failure

- Without government intervention it can lead to unemployment, a labour market failure

- Improving transport

- Incentivising

- Rationing

2) There are incentives to increase/decrease supply depending on if there is excess demand/supply

3) This increase/decrease in supply will ration away excess demad/supply taking us back to equilibrium

- Can opperate without the cost of people to regulate it

- Prices are kept low as resources are used as effeciently as possible

- Inequality in incomes and wealth as only those with purchasing power benefit from the price mechanism

*add to this

- Price regulation

- Profit regulation

- Performance targets and quality standards

- The CMA will carry out an investigation if a firm merging gives 25% or more market share or £70 Million in revenue. They will only be blocked from mergeing if they think they will negatively harm consumers

- RPI + K & RPI - X

- RPI - X allows for firms to increase their prices by the rate of inflation - x which is used to punish firms if they think they can be more effecient

- This can encourage firms to reinvest in new capital since then they cannot be taxed

- The Food Standards Agency (FSA) give out a quality standard as do the British Standards Institute (BSI) (childrens toys).

- Privitisation

- Helping small firms grow

- Stopping anti competitive practises

- By privitising firms the government create more competiton as now there is incentive form firms to make profit, forcing them to be effecient

- Private sector firms bid to win the contract, by offering the best deal - the highest quality for the lowest cost. The government then chooses the firm which offers the best value for money - and awards them the contract!

- Vertical intergration (forwards or backwards) is when firms take over other firms at different stages of the supply chain of the same product. By firms doing this they can create barriers to entry whereby other firms may struggle to access suppliers or retailers

- Price collusion, when 2 or more firms agree to restrict competiton

- R&D tax breaks

- Subsidies

- Increased competiton means improved efficiency and reduces x-inefefficiency

- Competiton may result in lower prices for consumers

- Government lose out on potential dividends since most privitised firms are often profitable

- Regulation to stop private monopolies

- Quality of regulation

- If the market is contestable and competitive

- Public sector is more likely to focus on welfare and provision of services

- Less likely to be market failures that arise from externalties

- Complacent and wasteful production = X-ineffeciency

- Expensive to run state companies and therfore there is a burden on tax payers

- Moral Hazard

- Politicians who make the decisions to nationalise firms will not suffer the burden if something goes wrong, taxpayers will

- If there is good regulation of private sector industries

- Level of competition: Nationalisation may not be needed if there is high levels of competition

- Higher incentive to minimise cost with more competition created, which leads to productive and X effeceincy

- Formation of oligopolies and local monopolies

- Just because legal barriers to entry are removed doesnt always make a market more contestable > consider strategic and technical barriers

- Levels of regulation on anti competitive behaviour

- Information gaps

- Distortion of the price mechanism

- Administration cost

- Illegalising goods creates black markets

- In 2002 the government wanted to make an NHS online database to improve effeciency, but 9 years later they didnt complete it because they lacked full information on the costs and technology. They ended up scrapping the project altogether wasting £11 billion in tax payers money

e.g. £21 Billion makes up the NHS's admin costs and it is estimated that 750 extra lives could be save every month if they could afford more medical supplies, despite a £150 billion budget

- Reduces innovation and dynamic effeciency

- Regulatory costs

- Effective for inelastic goods

- Government regulations are generally imposed to benefit the greater society = allocative effeciency and welfare gains

- Consumers may turn to black markets

- How effective is the minimum price (50p per unit of alchol)

- Black markets where consumers may be exploited by paying higher prices

- Low prices may mean lower quality goods

- Enforcement costs

- Stops monopolies from exploiting consumers

- Increase in consumer surplus

- Are they going to impact everyone equally (equitable)

- Regressive on lower income earning families

- Black markets/Tax evasion

- Increases the price of demerit goods, which discourages their consumption

- Encourages firms to change their behaviour e.g. making less sugary drinks

Ad Valorem Tax = Pivotal shift

- Moral hazard: firms might get complacent and wasteful

- Subsidies encourage investment = diverse products for consumers

- Prices are kept low for consumers

2) Government allocate permits based on the size of firm (Larger firm = more permits)

3) Will distibute permits until 10% of permits remain, which are then auctioned of to other firms

4) A firm must now either become more eco friendly or buy permits of other firms

- Pollution can be hard to measure = pollution cap may be wrong

- Relocation of firms to countries with low pollution regulation

- Market based = effecient allcation of permits

- Equitable for firms as it allows them to make choices

Legal monopoly = When a firm has 25% or more market share on there own and has the 'power' to act like a monopoly

- High barriers to entry/exit

- Imperfect information

- Differentiated product

- Firms are price makers

Allocatively inefficeint

X-inefficeint

Dynamically efficient

- Productive inefficiency: they do not produce where MC=AC either due to a lack of competitive drive meaning they dont necessarily have to, or diseconomies of scale whereby a monopoly grows too large

- X-inefficiency: complacent and wasteful production due to a lack of competitive drive

- Inequalities that arise in neccesity markets

- Greater economies of scale potential as monopolies are larger in size and as result we may see lower prices than in competitve outcomes

- Natural monopoly = If natural monopoly markets are regulated then they give society more desirable outcomes than if there was competition since it makes sence for that firm to dominate the market

- Objective of the firm = The theory states that the monopoly will profit maximise but what if they have other objectives that intend to bring about welfare in society

- Type of good/service = Necessity goods will have more extreme consequences if sold by a monopolist

- Huge economies of scale + first movers advantage

Any firms entering these markets would create undesired competition and a wasteful duplication of scare resources

MC = AR

Then the incumbent firm will set it price to AC so only normal profit is made causing the new firm to 'run' and leave the market

- Sunk costs

- Penalties for leaving contracts early

- Firm is a profit maximiser

- Many buyers and sellers (infinite)

- Perfect information of market conditions

- Homogenous goods

- X-efficiency

- Dynamically inefficient

- Large pool of potential entrants to the market

- Good information of market conditions

- Incumbent firms are subject to hit and run competition

- Increases the pool of potential entrants: firms can created new products and services disrupting current markets (uber, air bnb)

- Increased information : this allows for firms to learn about costs and market conditions

- Creation of jobs

- Creative destruction: new firms destroy old markets due to advancements in technology leading to job loss

- Anti competitve strategies may aries reducing contestability

- Role of technology (will it be used for good or bad, say to collect data on consumers which allows firms to practise price discrimination)

- Regulation

High barriers to entry/exit

Interdependence

Non-Price competition

Differentiated goods (Similar but slightly different)

- R&D

Tacit collusion is when firms limit competition without directly stating or formally agreeing and happens as a result of price leadership

- Predatory pricing = charging way below AVC to force other firms out of the market

- Limit pricing = when an incumbent firm sets prices so that other firms do not enter the market

- Loyalty Cards (Tesco clubcard, Nandos Card)

- Branding

- Quality

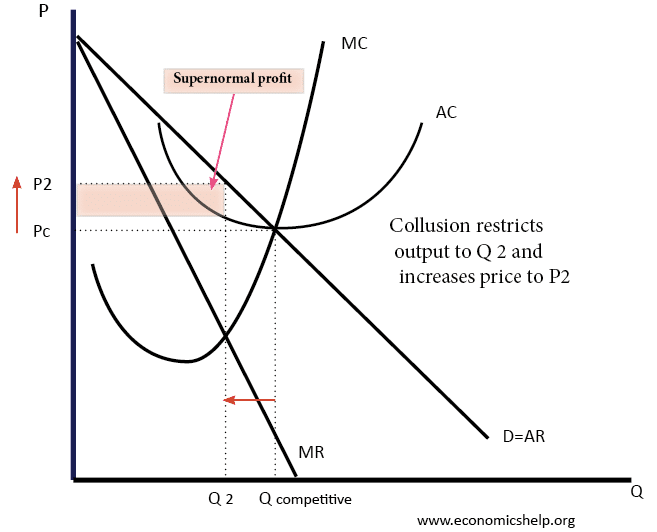

- Collusive = Will agree to restrict competition

- On the bottom section demand is inelastic. This is because if a firm lowers its price competitors will also match them hence demand doesnt change that much

- Oligopolies make supernormal profits which may mean they reinvest in R&D which can yield positive externalities

- When firms collude it may lead to a loss of consumers welfare since prices are raised and output is reduced

- The absence of competition could mean that there is a loss of efficiency gains

Artificial barries are created by the incumbent firm in order to reduce competition into the market e.g. predatory pricing, limit pricing vertical intergration

- Slightly differentiated goods (some price making power)

- Good information of market conditions

- Low Barriers to entry/exit

- Consumers get a wide variety of choice + competition drives prices low

- Short run supernormal profits may be enough to reinvest and bring small dynamic effeciency gains

- Although dynamic effeciency is not achieved in the long run, high levels of competition may mean that normal profits are reinvested in order to survive

- Dividends for shareholders

- Reward for entreprenership

- Workers

- Managers/CEO's

- Shareholders

- To avoid scrutiny by regulators, market authorities

- Key stakeholder is harmed as a result

- Sales Max

- Profit satisficing

- Increase market share, since market share is measured by revenue

- Principle agent problem

- This can lead to the principle agent problem when the agent (e.g. the manager who runs and controls the business) pursues different objectives to the principal (e.g. the shareholders who own the business)

- Generally shareholders will want to profit max while owners will want to revenue/sales max for bigger bonuses and to control a larger firm

- Limit pricing / Loss leader

- Economies of scale

- Principle agent problem

- Flood the market (develop loyalty then raise prices)

- Information to seperate the market into elastic and inelastic consumers

- Prevention of resales (market seepage)

eg at an auction

2nd = This involves charging different prices depending upon the choices of consumer. For example quantity, time period, collecting coupons

eg. family discounts at theme parks

3rd = When the market is segmented into elastic and inelastic consumers

-Strengthens the monopoly power of firms

- Inequalities

-It might cost a firm to divide a market, which might limit the profit that they can make in the long term

- Anti competitve practises

- Economies of scale- as firm can expand market

- Some consumers benefit (2nd 3rd degree)- Cross subsidisation

- This is also productive efficiency

How is it calculated?

MR x MP (MPP)

- In labour markets, we supply labour, and firms demand our labour

- This will lead to an excess supply of labour aka unemployment

- For those unemployed they will have no choice but to accept lower wages so that they can remain in work

- So wages will decrease, quantity supplied of labour will fall, quantity demand for labour will increase and the market will return to equilibrium

- For firms to hire workers, they must offer hire wages as a result

- This will lead to higher wages, quantity demaded of labour will fall and quantity supplied will increase

e.g. Mcdonalds til workers wanted higher wages they would significantly reduce QD, and replace them with self service machines

e.g. If superstar football players demand higher wages, teams need these players so they wont be very responsive in reducing demand

1) Substitutes (labour & capital)

2) PED for the product

3) % Of total Cost

4) Time

But if it is harder then demand for labour will be inelastic

When wages make up a lager % of a firms total cost demand for labour will become more elastic e.g. in a tutoring firm, tutors make up the majority of there costs, so if wages increased by alot, those firms would be significanlty effected since wages make up majority of there costs.

In the long run there is enough time for a firm to find substitutes when wages increase, making demand for labour elastic

e.g. If there was a large increase in wages for heart surgeon, supply would only increase by a bit since it is so heart to become a heart sugeon

e.g. if Mcdonalds increased wages there would be a significant increase in the quantity of labour supplied since it doesnt require much to work at Mcdonalds

- Unemployment levels

- Time

The less skills and qualifications you need the more elastic the supply of labour is

Lower unemployment means that when there is an increase in wages, there will be a smaller % increase in the number of people willing and able to work since most people will have jobs i.e inelastic supply

In the long run supply will become elastic because there’s lots of time to apply and train for the job so if there is an increase in wages workers are likely to be more responsive

2) Self employed goes against the theory

3) MRP takes the assumption that labour markets are perfectly competitive, trade unions may bargain for higher wages, which has nothing to do with a workers MRP or monospsony with lower wages

- Change in the final price of the product labour is making

- Change in demand for the for the final product

- Change in labour productivity

- Change in the price in capital

If demand for a good is elastic and wages go up, they cant pass these costs on to consumers since this will cause TR to fall, so more workers may be fired i.e. reduced demand for labour

- When wages rise from a low level, an individuals supply of labour increases since an individual is more willing to work at higher wages to improve there standard of living (+ income effect, + sub effect)

- As wages rise, the opportunity cost of lesiure time rises, but individuals begin to reach a level of income that they are happy with, so num of hours worked reduces (- income effect)

- When the curve bends back on itself, we assume at this point individuals have reached their target income, so even with higher wages they wont be willing to work more and give up leisure time.

- Size of the working population

- Overtime

- Improvements in occupational mobility of labour

- Non pecuniary benefits (fringe benefits, long holidays, employee discounts)

- Different wages in substitute occupations

- Labour is homogenous

- There is perfect information (workers know the wages, firms know how good workers are)

- Firms are wage takes

- No barriers to entry/exit

- If we dont get wage differntials in perfectly competitve labour markets, then we can learn that there must be things going wrong with real world labour markets

2) Labour is not perfectly mobile (Geographical, occupational, lack of information)

3) Non-monetary considerations (In perfectly competitive labour markets the assumption is that workers base the choice to work one wages alone)

4) Trade unions and supply restriction

5) Monopsonies and wage setting ability

- e.g. Teachers, Nurses (UK) Mcdonalds, Walmart

- Hire up to where MRP=MC(L)

- Reduce employment & Wages

This implies that the MC(L) will be greater than the AC(L)

- Workers are payed a wage (Wm) much lower than there MRP

1) The trade union will bargain for a higher wage, above the competitive wage

2) At that wage there is a limit to the number of workers happy with the wage rate, shown by the existing supply curve

3) This is because all the workers below that point would of already been happy with a wage below the TU wage since thats what they had been working for

4) Beyond that point the employer would have to raise wages in order to attract in more workers

5) Wages will rise and there will be excess supply of labour (unemployment)

- They increase unemployment, real wage unemployment

- Depends on the strength of the trade union (how large the union is)

- The real world shows us that trade union strength is actually very limited

- Restructuring of the UK economy: Movement away from large manufacturing jobs where people would work under 1 firm, to service sector jobs, which makes it alot harder to organise trade unions

- Competitve pressures: Firms can reject trade union wages in order to keep their costs low and remain competitive

1) Trade unions will bargain for a wage above Wm

2) The monopsonist becomes a wage taker up until a limit, because there is a limit to the number of workers willing to work at that new wage rate

3) The supply curve will also become the MC(L) and AC(L) until that limit

4) At that limit the monopsony must increase wages to attract more workers. But the key is thats not just for the next worker its for every other worker that follows, so the MC(L) will revert back its shape

5) Employment and wages will increase as a result of this TU

For 23 and over it will increase in April 2024 to £11.44 an hour (from £10.18). This will account for a £1800 increase a year for 2.7 million workers.

- Fiscal benefit to the government (Reduced benefits payments + Tax revenue from people working)

- Boost in morale > workers become more productive

- Improve inequality, reducing the gap between the rich and the poor

- Can cause cost-push inflation because of increased production cost

- Unattractive to FDI if NNW is too high, since there is no point of outsourcing in the UK with higher costs

- Can cause other pay groups to request higher wages, further increasing costs, and leading to wage push inflation

- Is it high enough to incentivise those on benefits to join the labour force

*Add to*

- A monopoly can choose any price and output between MR=MC and normal profit

- As a result the day to day running of the firm is done by the owners seeking profit

- But as a firm wishes to expand production, they will need to raise shares.

- Firms will sell shares to raise funds and expand, but in the process the ownership gets diluted

- As a result larger firms will become dependent on specialist managers who are employed to run the business on behlaf of the shareholders

The union claims strikes in 2023 cost the economy £5bn, with the the lesuire sector taking the greatest impact from the loss of sales.

£700m revenue lost from the rail industry

- Long-term investment in education and training to prepare people better for the labour market.

- Structural reforms to promote stronger and more sustainable economic growth which can boost demand for workers, creating a more competitive environment that forces managers to drop discriminatory hiring and promotion practices.

- Specific anti-discrimination legislation backed up by effective enforcement.

- Enforcement agencies should be empowered, even in the absence of individual complaints, to investigate companies and sanction employers when they find evidence of discrimination

- The Equality Act 2010 The Equality Act brought together different acts outlawing different types of discrimination – age, sex, disability, religion, sexual orientation.

The market can fail to end discrimination if:

- Government legislation enforces discrimination (apartheid laws US, South Africa)

- Discrimination occurs amongst consumers too.

- If firms have monopoly power – despite higher costs of discrimination, barriers to entry prevent new non-discriminatory firms from entering the market.

- Discrimination – pre-labour market. One major cause of wage differentials is not discrimination by employers but different life chances and education of people entering the labour market. If black-Americans have fewer qualifications than average, economic theory would predict that even with non-discriminatory employers, average wages would be lower for certain groups.

{kind=link}