Chapter 1 - 8 pre exam questions Flashcards

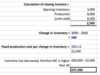

Calculate the over / under absorption using the following data.

Contribution is a key concept of marginal costing.

- What is it used for?

- How is it calculated?

- For every unit of inventory sold, contribution per unit is the amount of revenue generated to pay off fixed overhead costs.

It is used to help with short term desicion making → E.g If a business has a one of order or spare capacity.

Production budget

What is the formula to calculate it?

Budgeted production = forecasted unit of sales + closing inventory - opening inventory

Material budget

What are the two types of material budget and how are they calculated?

- Material usage budget = Budgeted production for each product x Number of Kgs required to produce one uint of the product

- Material purchase budget = Materials usage budget + closing inventory - opening inventory

- What is a master budget?

- What does is nomally contain?

- The budget into which all subsidary budgets are concolidated → it is drawn up after all the funtional budgets have been approved.

- budgeted profit & loss account / balance sheet / cash flow statement.

What are the 2 methods for analysing semi-variable costs into fixed and variable elements?

- High - low method → estimates fixed and variable costs of a production / service

- Least squares regression → establishing a cost equation using a line of best fit (y = a + bx)

Give the equation for working capital

Working capital = Current assets - current liabilities

(= Inventory + recievables + cash + short term investements- payables - liabilities)

- What is a cash budget?

- What are the 2 main aims of it?

- What is not included in a cash budget?

- A budget of estimated futre cash reciepts and payments to show the forecast cash balances of a business and different intervals.

- To help managment make forward planning decisions (advicing bank on overdraft estimates) / to anticipate cash shortage or surpluses

- Non cash items (e.g. depreciation / debt write off’s / valualtion of assets)

Hopwood researched styles to evelate managment performance… explain the following and the efects on behaviour

- Budget constrained style

- Profit conscious style

- Non accounting style

- Evaluating managers success in meeting budget targets short term → high pressure / data manipulation

- Measures a managers ability to increase overal effectivness more long term (cutting costs) → Less pressure / manipulation. Better relationship between management and staff.

- Similar to profit conscoius style with a lower concern for cost

- What is an investment centre and in what 2 ways is it measured?

A profit centre with additional responsibility for investment and financing

- % Return on inevestent (ROI or ROCE) = (Profit / capital employed) x 100

- Residual income (RI) = profit - % of capital employed

Give the equation to calculate the rate of inventory turnover.

COS / Avergae inventory

What is a balanced scorecard?

A development to translate a copanies objectived into perfomance measures to manage muliple objectives.

A balanced scorecard for a company would be contructed by considering 4 perspectives, what are these?

- Financial → How do we create value for shareholders.

- Customer → What is it that the customers value

- Internal → what processes will achieve our financial and customer objectives.

- Innovation & learning → how can we improve and create future value.

- What is a Critical Success Factor (CSF)?

- What is a Key Perfomance Indicator (KPI)?

- Things a business must get right to succeed in relation to a given perspective. <em>(Previous Q)</em>

- The way in which CSFs can be measured.

What is a budgetary control cycle?

Comparing the paln of a budget to the actual results and investing any significant differnces.

What are the benefits and problems with balanced scorecards?

Benefits

- Provides external and internal infomation

- Focuses on factors that will enable a company to succeed.

Problems

- Selection of measures

- Obtaining infomation

- Infomation overload

- Conflict between measures.

- Give 2 things normalling contained in batch costing

- Give 2 things not normalling contained in batch costing

- Actual material cost & Absorbed Manafacturing overheads

- Actual manafacturing overheads & Budgeted labour costs

- What is a sales price varaince?

- How is it caluclated in terms of an adverse or favourable profit?

- The effect on contribution due to the actual selling price being differnet from that budgeted.

2.