605: Week 13 Flashcards

(23 cards)

What criteria would be useful in evaluating current and future health reform to assess impact (5)?

Access to care, cost, financing, equity, and sustainability

Access to care: how comprhensive is coverage? how is insurance coverage acquired (employer, individual, gov’t)? autonomy to select providers/# of providers? do copays restrict overall access or certain providers?

Cost: How much does it cost individuals for insurance and services? How does reform affect health costs overall? Control future cost increases? Affordable for businesses/population/government?

Financing: How will reform be financed? Where will the money come from (taxes?)? Change payments to hospitals and MDs? Provider response to these changes? Subsidies to low-income populations (e.g. as with policies purchased in State Exchanges under ACA)?

Equity: Is reform fair to all individuals? How do we judge fairness? Equity in financing (regressive vs. progressive tax)?

Sustainability (long run): Designed to live within budget so programs don’t go broke? Systems to monitor regularly, make changes?

The Patient Protection and Affordable Care Act (PPACA)

Patient Protection and Affordable Care Act (PPACA)

- Often referred to as ACA

- Legislation passed March 2010 (when Democratic majority in House and Senate)

- Narrowly passed (219-212 vote)

- No Republican voted for it

- Complex legislation; many individual components

- Several challenged in court

Broad goals of ACA

- Expand access to health insurance coverage

- reduce # of uninsured

- Increase consumer insurance protections and improve coverage for those with insurance

- Insurance reformes (e.g. can’t deny those with pre-existing conditions or resciend policy when a person is ill, etc.)

- Improve health quality and system performance

- Control rising healthcare costs

Selected ACA features by year: 2010

- Children <26 y.o. remain on parents’ policy

- Children cannot be denied insurance due to pre-existing conditions

- Adults may still be denied insurance for this reason until 2014, but may enroll in temporary federal high-risk pool

- Bans lifetime $ limits of insurance policies (annual limits banned in 2014)

- Adds certain preventive benefits with $0 copay

- 10% tax on indoor tanning services

- Federal grants: (to enhance prevention of disease)

- Prevention & Public Health Fund; comparative effectiveness research

Selected ACA features by year: 2011

- Improved Medicare prevention benefits (including free general exam during 1st 12 months; $0 copay)

- New Center for Medicare and Medicaid Innovatin (CMMI) to test new payment/delivery models that decrease cost

- Minimum Medical Loss Ratio (MLR) = 85% (large group market); = 80% (individual and small group market)

- Insurance companies have to pay at least 85% (if large group market) out in the form of benefits payments - if they don’t end up paying out that percentage of the income from premiums then they have to pay money back to beneficiaries in the form of rebates (a way to keep insurance companies from raising prices too high just for profit)

- MLR = % of total premium income paid out in benefits

- Individuals receive rebate if MLR < minimum levels

- pre-2014 % of premium income not paid out was higher than this for most big insurance companies (in contrast Medicare only had 1.3% not paid out) - see attached diagram

- Insurance companies have to pay at least 85% (if large group market) out in the form of benefits payments - if they don’t end up paying out that percentage of the income from premiums then they have to pay money back to beneficiaries in the form of rebates (a way to keep insurance companies from raising prices too high just for profit)

Selected ACA features by year: 2012

- Accountable Care Organizations (ACOs) - share savings

- ACOs are integrated groups of providers

- These organizations are intended to coordinate patient care, improve quality, reduce unecessary hospital admissions, increase efficiency

- If they reduce costs, they can keep part of savings

- New value-based purchasing program for Medicare

- Amount paid to hospitals based partly on quality measures

- Hospital payments reduced for “preventable” readmissions

Selected ACA features by year: 2013

- New 2.3% tax on sale of medical devices

- Controversial - attempts to repeal (bipartisan dislike of this tax)

- Decreases Disproportionate Share Hospital (DSH) payments by Medicare and Medicaid when hospitals treat large % of Medicaid and uninsured patients

- Since there will hopefully be a decrease in uninsured patients, hospitals shouldn’t need this small payment anymore since they will be making more from insurance

Selected ACA features by year: 2014

MAJOR changes:

- Expand Medicaid coverage

- Medicaid coverage expanded to all non-Medicare with income < 138% FPL (originally 133% but new rules of calculating income results in 138% FPL cutoff)

- Federal gov’t pays 100% of cost of newly eligible Medicaid beneficiaries 2014-2016; falls to 90% by 2010.

- Original legislation required states to expand Medicaid eligibility to risk federal funding for currently-eligible Medicaid beneficiaries

- Supreme Court ruling allowed states to continue current Medicaid program but have option to decline expanding Medicaid eligibility (the one part of the law that got overturned by the Supreme Court)

- Medicaid coverage expanded to all non-Medicare with income < 138% FPL (originally 133% but new rules of calculating income results in 138% FPL cutoff)

- New Health Insurance Exchanges for individuals

- State health insurance exchanges sell policies to individuals & small businesses (another avenue for individuals to buy insurance)

- Also make things more transparent - display information about benefits, costs, etc. in a way that is easily understandable

- States can “opt out” of developing own health insurance exchange. These states served by Federal insurance exchange (opened 10/1/13 with many web problems)

- 4 categories of insurance plans

- Difference is % of estimtated health costs covered by policy (Bronze = 60%; Silver = 70%; Gold = 80%; Platinum = 90%)

- Premium higher and copayments lower (lower cost-sharing) as the % of health costs covered by policy increases

- Premiums may vary due only to following factors: age (older insured pay no more than 3x lowest cost); family size; geographic area; tobacco use (allows 50% higher for smokers - CA declined to allow this variation)

-

Premium subsidies for those purchasing through insurance exchange and have income 138% - 400% of FPL

- $ amount of subsidy decreases as family income decreases

- Beyond 400% FPL, can still purchase insurance policy from State Exchange, but don’t get federal subsidy (recent Supreme Court challenge to legality of subsidies for policies sold through Federal Insurance Exchange - legality was upheld)

- Individual mandate

- Individuals must have insurance policy (that has defined minimum benefit package)

- Penalty if not:

- 2014: $95 per adult or 1% of family income, whichever is greater

- 2015: $325/adult or 2% family income

- 2016: $695/adult or 2.5% family income

- Necessary to enroll enough (low-cost) younger and healthier people to offset higher costs of newly-insured (high-cost) people (pre-existing conditions, etc.)

- Individual mandate not new idea

- Republican counterproposal to Clinton health bill

- Important component of Gov. Mitt Romney’s health reform in Massachusetts

- Other features:

- Adults cannot be denied insurance coverage due to pre-existing conditions

- No annual $ limits on coverage (lifetime limits banned in 2010)

- Decreases Medicare payments by 1% for hospital-acquired conditions

Selected ACA features by year: 2015 and 2018

2015

- Employer Mandate

- Requires employers with >50 full-time employees to provide “acceptable” insurance

- Penalty = $2000 per F-T employee

- Originally supposed to be implemented in 2014, but was delayed to 2015

2018

- New tax on “Cadillac” employer-provided insurance plans with very comprehensive coverage

- Implications: inject more cost-sharing into consumer decision making

- Poll showed that 60% of people oppose this tax, but this % changes when questions about the support of the tax are posed in different ways (e.g. if it decreases overall healthcare costs more people are for it)

Current status of State individual marketplace and Medicaid expansion decisions

- There are only 17 states (including DC) with fully state-based health insurance exchange (mainly states in West and NE); all others use Federal exchange

- 20 states have NOT agreed to expand Medicaid eligibility

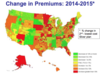

Change in premium costs between 2015 and 2016 (U.S. average - unweighted and unweighted)

Changes in insurance company participation in the exchange marketplaces

Changes in premium costs between 2015-2016

2nd lowest cost monthly silver premiums

(40 y.o. non-smoker making 30K/yr)

- U.S. Average (2015-2016): unweighted % change 10.1%

- U.S. Average (2015-2016): weighted (by enrollment) 3.6% (reflects who is actually buying policy - small number might be buying higher cost premiums)

Changes in insurance company participation in the exchange marketplaces

40% of counties in states using Healthcare.gov will have only 1-2 insurers in 2016 (not as much choice)

- increase from 35% with 1-2 insurers in 2015

- most of these in rural areas

% of all counties:

- 36% losing 1 or 2 insurers in 2016

- 17% gaining 1 or 2 insurers in 2016

Implications for premium competition?

With ACA who will remain uninsured (and how many)?

Congressional Budget Office (CBO) estimate 23 million uninsured 2019 (and this is an underestimate b/c so many states didn’t expand Medicaid)

Who?

- Immigrants who are not legal residents

- Eligible for Medicaid but not enroll

- Exempt from mandate

- Most can’t find affordable coverage

- Choose to pay penalty in lieu of buying insurance

Public opinion on ACA

Opinion on what Congress should do (expand the law, more forward with current law, scale back law, repeal law entirely) - Total and Democrats v. Independents v. Republicans

Of the percent of people who say the ACA should be repealed, what do they think should be done if that occurs?

Public opinion for and against ACA about equal at the moment (much wider gaps in 2013 and 2014)

Opinion on what Congress should do about ACA law:

Total: 25% for expanding the law; 18% for moving forward with how it is; 11% think it should be scaled back; 31% think the law should be repealed entirely

Democrats more for keeping/expanding law; Republicans way more for scaling back/repealing; Independents about half and half for and against

What to do if ACA repealed?

Of the 31% of people in U.S. who say Congress should repeal entire law:

- 11% think that it should be replaced with a Republican-sponsored alternative

- 13% think that the law should not be replaced (this is 42% of those saying the ACE should be repealed)

Financing the ACA

- 2010-2019 ACA financing (Federal savings vs. new revenues)

ACA funded from combination of additional revenues and anticipated cost savings

- Additional costs:

- insurance coverage provided to many currently without insurance

- additional benefits (services covered)

- Presumed cost savings from changes in delivery system to increase efficiency

Financing ACA: 2010-2019 (major ones):

- Federal Savings:

- Medicare Advantage reductions $332 B - lower payments to Medicare HMOs

- New Revenues:

- Individual and employer penalty payments $69 B

- Medicare tax $210 B - more taxes paid by high-income beneficiaries

- Health industry fees $107 B

- High-cost insurance tax (Cadillac insurance) $32 billion

Legal challenges to ACA

- Suits brought in many state challenging constitutionality of ACA

- All but 2 federal court decisions supported constitutionality of ACA (Medicaid expansion and individual mandate - but individual mandate later upheld in Supreme Court)

- Supreme Court agreed to hear case

- Justice Sotomayor urged to recuse herself since she worked on the development of ACA; but she stayed, saying she could be unbiased

- Ruling on 6/28/12 - most of ACA ruled constitutional (5-4 vote)

- Conservative Chief Justice Roberts emerges as “savior” of individual mandate (sided with liberals)

- Court rejected federal authority of individual madate under Commerce Clause (i.e., cannot force individuals to buy a product), but upheld individual madate by framing the penalty for refusing to buy insurance as a tax that Congress does have power to regulate using its taxing authority

- Court decided that threatening to withhold all Medicaid funds from states that reject Medicaid expansion is unduly coercive and unconstitutional

- Medicaid expansion exerts such a profound change on nature of the law that should be treated as a new and optional program for states

- States now are given the option whether to expand Medicaid up to 138% FPL (problem: this was the major way to increase coverage under ACA)

- If state decides not to expand Medicaid to 138% FPL:

- eliminates coverage for poorest residents (family incomes 100%-138% FPL) - ACA presumed these would be covered by Medicaid expansion so no provision covering for them otherwise

- tax subsidies to purchase insurance through Exchange not available to uninsured persons with family incomes 100%-138% FPL

Specific legal challenges:

- Is this (i.e., 2012) the time to decide on constitutionality or wait until major provisions implemented in 2014?

- Does individual madate exceed federal power under constitution?

- Argument: Commerce Clause provides right to regulate economic activity; but forcing some to purchase insurance when otherwise would not amounts to regulating inactivity

- If individual madate is unconstitutional, is it separable from the ACA or does that mean the entire ACA should be ruled as unconstitutional?

- Is ACA clause requiring states to participate in Medicaid expansion or risk federal dollars for current (pre-ACA) Medicaid program constitutional? (Ruled unconstitutional)

New Supreme Court challenge:

- Supreme Court heard challenge this year on constitutionality of federal subsidies provided to those who purchase insurance in Federal Insurance Marketplaces

- Original legislation provided for federal subsidies only if purchased in State Insurance Exchange

- Would undermine objective of increasing insurance coverage

- Ruled constitutional

The future of the ACA

- Congressional attempts to:

- Repeal entire ACA

- Difficult even if Republican Senate and President in 2016

- Roll back some provisions (e.g. medical device tax)

- Deny funds needed to implement some provisions

- Repeal entire ACA

- More lawsuits?

- Large % of American public still opposes ACA

Tracking impact of ACA

- Reduction in total # uninsured?

- Change in premiums of policies on exchanges or private (group) markets?

- Change in copayments and other insurance provisions?

- Change in out-of-pocket expenditures by population?

- Change in # people paying penalty for no insurance?

- Change in insurance provided by employers? Increased layoffs?

- Change in F-T employment?

- Change in # states participating in Medicaid expansion &/or having own Exchange?

- Change in rate of increase in health costs over time?

Importance of economic evaluation of proposed programs

Why perform economic evaluations?

Economic evaluations: objective way to compare and evaluate alternative ways of using resources to improve health

Why perform economic evaluations?

- Identify best use of scarce resources

- Limited funds available to improve health of some targeted population, need to find best way to use those funds (just because programs have large positive outcomes, that doesn’t necessarily mean they shoudl be implemented - could be too costly to be worth it)

- Spend funds to yield maximum health improvement possible

Alternative economic evaluation methods

Deifferences in evaluation methods?

- Cost Analysis

- Efficacy or Effectiveness Analysis

- Cost Minimization Analysis

- Cost-Benefit Analysis (CBA)

- Cost-Effectiveness Analysis (CEA)

- Cost-Utility Analysis (CUA)

Differences?

- Focus only on program costs or outcomes

- If full economic evaluation, comparing both costs and outcomes of multiple programs

- Are outcomes equivalent or different?

- Are outcomes measured in $ or nonmonetary terms?

- If nonmonetary outcomes, adjust for quality?

- Cost analysis - focuses only on costs

- Efficacy or Effectiveness analysis - focuses only on outcomes

- Cost minimization analysis - focuses on both costs and outcomes, but only for programs that have equivalent outcomes (so pick program that costs less and has same outcomes)

- Cost-benefit analysis - focuses on both costs and outcome, but only considers monetary units for both cost and outcome ($ costs vs. $ benefits)

- Cost-effectiveness analysis - focuses on both costs and outcome, but considers non-monetary outcomes (e.g. cost per additional year of life); does not adjust for quality

- Cost-utility analysis - focuses on both costs and outcome, consideres non-monetary outcomes, adjusts for quality of outcome (e.g. cost per additional QALY - quality adjusted life year)

Cost-benefit analysis (CBA)

- Definition

- How results are displayed (including equations)

- Example

- Advantages

- Disadvantages

Cost-benefit analysis: compares $ costs and $ benefits

- Results displayed one of following:

-

Net benefits

- total benefits - total costs

- If > 0, good program!

-

Benefit-Cost Ratio (or Cost-Benefit ratio)

- $ benefits / $ costs

- $ benefits (e.g. cost savings) per $1 cost

-

Net benefits

Example:

– Suppose program cost = $2,250,000

– Total $ benefits estimated to be $4,000,000

• Results:

Net Benefits: Total $ benefits – Total $ costs

= $4,000,000 - $2,250,000 = $1,750,000

• Interpretation: Benefits exceed costs by $1.75 million

B/C ratio: Total program $ benefits / Total program $ costs = $4,000,000 / $2,250,000 = $1.78

• Interpretation: Every $1 the program costs yields $1.78 in benefits (e.g., lower health costs)

Advantages:

- Can evaluate 1 program (doesn’t need to compare to another program to interpret results)

- Should it be implemented? Yes, if $ benefits > $ costs (or if B/C ratio is > 1)

- Consistent with how people often approach decision making (i.e. how much “return” for each $1?)

- Can evaluate programs with different health outcomes

- convert outcomes into $; compare net benefits or B-C ratios

Disadvantages:

- All benefits of programs (e.g. saving lives) valued in $ (controversial)

- How to value saving a life in $?

- Current measures rely on lifetime earnings (which means lower-income people are valued at less)

- May undervalue lives of certain populations

- How to value saving a life in $?

Cost-Effectiveness Analysis (CEA)

- Define

- Measures used

- Equation

- Interpretation

- Example

- Advantages

- Disadvantages

Cost-effectiveness analysis: compares $ costs with non-monetary measures of health outcome

Measures used:

- Benefits of program are NOT measured in $ (as opposed to cost-benefit analysis)

- Use other measures of health outcomes

- Often called health effects or health outcomes

- Examples:

- # years of life saved (i.e. # additional years of life)

- Reduced # disability years

- Reduction in cholesterol or BP

Equation: (using examples of measures that could be used)

Total program cost / total # life years saved

Interpretation: Cost of program per additional year of life saved

Example:

If program cost is $2.25 million and saved total of 300 years of life:

CEA = $2,250,000 / 300 = cost $7,500 per year of life saved

Advantages:

- No need to place $ value on human life

- Health effects measured in non-$ units; not % cost savings

Disadvantages:

-

Can’t evaluate if 1 program is “worth” implementing (e.g. if benefts > costs)

- so often have to compare one program with another

- Just counts # outcomes; doesn’t adjust for quality

-

Can’t compare programs with different outcomes and different measures of health effects

- e.g. Program A costs $4500 per 10-point reduction cholesterol. Program B costs $8000 per additional hour weekly exercise.

Cost-Utility Analysis (CUA)

- Define

- Measures

- Interpretation

- Calculation

Cost-utility analysis: a variation of cost-effectiveness analysis

- Cost-utility compares $ costs with non-monetary outcomes but also further adjusts for quality of outcome

- e.g. cost of program per additional quality-adjusted life year (QALY)

- QALY = adjusts years of life saved by the quality of those years

Measures used:

Calculate QALYs:

- As before, program saves 300 years of life, but . . .

- 150 years at full health

- 75 years at 80% of full health

- 75 years at 40% of full health

- Then QALYs = (150 x 1.0) + (75 x 0.8) + (75 x 0.4) = 150 + 60 + 30 = 240 QALYs

- So even though program saves 300 total years of life, these equate to only 240 QALYs (i.e. full-health years) - 60 years “lost” due to 150 of 300 years spent in less than full health

Interpretation:

Cost of program per additional QALY

Calculation:

CUA = total program cost / total # QALYs

=$2,250,000/240 QALY

=$9,375 per QALY

*Note: the program costs more per QALY than it costs per additional life year saved (with cost-effectiveness analysis) b/c not all years of life are at full health

Advantages:

- Doesn’t value life in $ (same as CEA)

- Allows comparison of programs with different objectives (like CBA) - since all compared to a single outcome measure: QALYs

Disadvantages:

- Cannot evaluate 1 program - have to compare to another program (like CEA)

Summary of economic evaluation

Cost benefit analysis

- Net benefit of $1,750,000

- $1.78 benefit per additional $1 cost

Cost-effectiveness analysis

- $7,500 cost per additional year of life saved

Cost-utility analysis

- $9,375 cost per additional QALY