5 Consolidations and Segment Reporting Flashcards

(50 cards)

What is the IFRS 3 definition of business combination?

Transaction or other event in which an acquirer obtains control of one or more business.

What is the IFRS 10 definition for control?

A parent is exposed, or has rights, to variable returns through its involvement with the subsidiary and has the ability to affect those returns through its power over the subsidiary.

How does power arise?

Power arises from rights (e.g., voting rights attaching to shares), or one or more contractual arrangements. De facto control.

Define acquisition

The accounting method used for business combinations (IFRS 3).

What are the 5 bases for acquisition accounting?

Who is the acquirer and who is the acquiree?

When is the acquisistion date?

Purchase price.

Recognition and measurement of assets, liabilities and non-controlling interest.

Accounting for goodwill.

Define goodwill

Future economic benefits arising from other assets acquired in a business combination that are not individually identified and separately recognised.

What comes under goodwill?

(name 5)

Workforce, reputation, innovative capacity, market power, synergy possibilities, etc

Example: P bought 100% of the shares of S at a purchase price of £100,000. The book value of the net assets of S at the acquisition date according to the balance sheet of S was £70,000. The fair value of the net assets of S at the acquisition date was £80,000.

Explain how to calculate the goodwill on consolidation in accordance with IFRS 3.

100% of the shares for £100,000.

As we are dealing with transactions, we are concerned with fair value not book value.

Goodwill = £100,000 - £80,000 = £20,000

Goodwill equation

Goodwill = Purchase price - (fair value of assets - fair value of liabilities)

How is goodwill measured after recognition?

(IFRS 3)

Measured at cost less any accumulated impairment losses (not amortised).

How is impairment recognised for goodwill?

(IFRS 3)

Treated for impairement annually, or more frequently if events or changes indicate that it might be impaired (consitent with identifiable intangible assets with indefinitite lives).

What is non-controlling interest?

When the acquirer buys less than 100 percent of the shares of the acquiree, there is a part of ‘non-controlling interest’ in the acquiree.

How is NCI measured?

(2)

The non-controlling interest’s proportionate share of the acquiree’s identifiable net assets at fair value (consider NCI does not get affected by goodwill).

Fair value: consider the purchase price allocation will be based on the purchase price that the acquirer would have paid if it acquired 100 percent of the shares.

Example: P bought 70% of shares of S at purchase price of £180,000. The fair value of the net assets of S at the acquisition date was £200,000. If P had acquired 100% it would have been £250,000.

Calculate the goodwill using proportionate net assets.

Purchase price: 180,000

Net assets @FV (200,000*0.7) = 140,000

Goodwill = 180,000 - 140,000 = 40,000

Example: P bought 70% of shares of S at purchase price of £180,000. The fair value of the net assets of S at the acquisition date was £200,000. If P had acquired 100% it would have been £250,000.

Calculate the goodwill using proportionate NCI.

Purchase price = 180,000

NCI (200,000*0.3) = 60,000

180,000 + 60,000 = 240,000

Net assets @FV = 200,000

Goodwill = 240,000 - 200,000 = 40,000

Example: P bought 70% of shares of S at purchase price of £180,000. The fair value of the net assets of S at the acquisition date was £200,000. If P had acquired 100% it would have been £250,000.

Calculate the 100% value and net assets.

Purchase price (100%) = 250,000

Net assets @FV = 200,000

Goodwill = 250,000 - 200,000 = 50,000

Example: P bought 70% of shares of S at purchase price of £180,000. The fair value of the net assets of S at the acquisition date was £200,000. If P had acquired 100% it would have been £250,000.

Calculate the 100% NCI and net assets.

Purchase price = £180,000

NCI (250,000-200,000) = £50,000

£180,000 + £50,000 = £230,000

Net assets @FV = £180,000

Goodwill = £230,000 - £180,000 = £50,000

What is the rationale for consolidated financial statements?

They are one economic entity.

Recognition and measurement for consolidated accounts.

(5)

- recognise and revalue the acquired net assets to fair value at acquisition date

- calculate the goodwill, eliminate investment of the parent on the subsidiary and add in the goodwill on consolidation

- only include the parent share of the post-acquisition profits in the consolidation

- recognise inter-company trading and eliminate unrealised profits

- include non-controlling interest

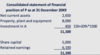

PPE row on the consolidated statement 31 Dec 20X9

25,000 + 6,000 = 31,000

Goodwill row on the consolidated statement 31 Dec 20X9

9,000 - (80%*6000) = 4,200

Current assets row on the consolidated statement 31 Dec 20X9

11,000 + 2,000 = 13,000

Share capital row on the consolidated statement 31 Dec 20X9

30,000

Retained earnings row on the consolidated statement 31 Dec 20X9

15,000 + [80%*(3000-1000)] = 16,600